OPEC to Pause Oil Production Increase After Earlier Boost? The Oil Surplus Crisis May Be Resolved, and Oil Prices Are Set for a Rebound!

بواسطة Linh Nguyen

تم التحديث: 9 Mar 2026

المقالات الشائعة

OPEC and its allies will pause production increases after boosting output to stabilize oil prices. The future of oil prices looks stable!

The Organization of Petroleum Exporting Countries (OPEC) and its allies, a super group of oil producers, reached a consensus at their monthly meeting: starting in December, they will slightly raise their oil production target by 137,000 barrels per day. However, OPEC+ also announced that it would suspend any production increase plans entirely in the first quarter of 2026.

OPEC+'s official stance remains firm: the global economic outlook is stable, and the fundamentals of the oil market are as healthy as ever. However, the first quarter is traditionally a low-demand period for oil, and weak consumption is almost certain.

On the surface, this pause in production increases is a rational response to seasonal factors. In reality, it reflects the alliance's cautious optimism about the future supply-demand outlook.

Hidden behind this decision is a subtle balancing act concerning the uncertainty of global oil demand growth — trying to avoid oversupply by not easing too soon while maintaining enough production to stabilize oil prices.

In OPEC’s October monthly report, the organization confidently predicted that global oil demand would grow by 1.38 million barrels per day in 2026, with supply and demand reaching a balanced state. In contrast, the International Energy Agency (IEA) reported the same month that demand would only grow by 700,000 barrels per day, with the supply side possibly facing explosive increases, resulting in an astonishing surplus of up to 4 million barrels per day.

The significant discrepancy between these two major institutions’ forecasts not only highlights the ideological divide behind the data but also adds layers of uncertainty to OPEC+'s decision-making process.

OPEC+'s decision to pause production increases is essentially a preventive insurance strategy, aiming to block the potential price collapse triggered by an oversupply.

Recently, the US imposed new sanctions on Russian oil producers, while President Trump continues to pressure Russia’s major oil buyers, India and China. This has led to market concerns about possible disruptions in Russian oil supplies. In the short term, Indian and Chinese purchases may decline, but it is generally expected that this is only a temporary issue, and Russian oil exports will soon return to normal.

The demand lifeline for oil in Asia is controlled by China and India, the two largest net oil importers in the world, and they are highly sensitive to oil prices. When prices are reasonable, they stock up heavily; when prices rise, they immediately cut back on imports.

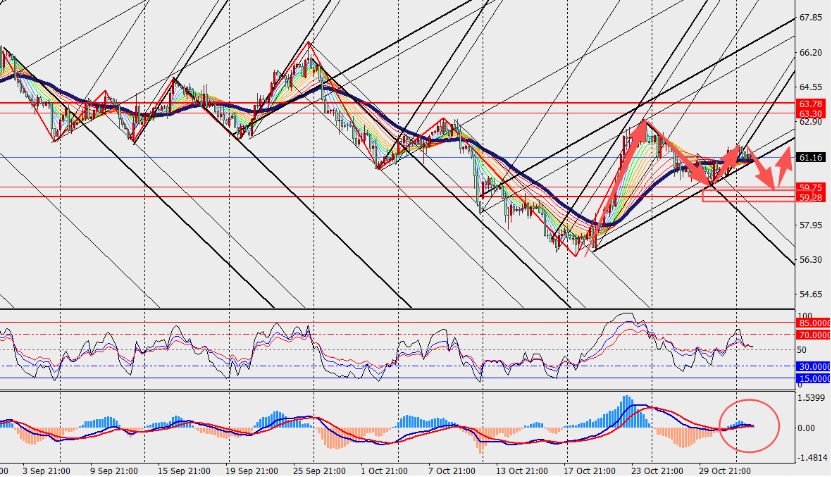

Market Interpretation:

On the 4-hour chart, crude oil remains in a range, with the MACD lines and volume bars near the zero axis, showing shrinking momentum. Optimism on the supply side mainly comes from Russia’s resilient export capacity and the ongoing production expansion of non-OPEC oil-producing countries. On the demand side, the situation heavily depends on the Asian market, the largest oil import region in the world, which accounts for about two-thirds of the total oil transported by sea.

Linh Nguyen brings 11 years of energy markets expertise with a degree in Petroleum Engineering and certification in Energy Risk Management (GARP). Her coverage includes crude oil, natural gas, and renewable energy markets with a focus on geopolitical factors. Linh is also an established writer, producing market outlooks and research articles for energy traders and contributing to specialized energy reports.

اقرأ المزيد