Trump’s Visit to Japan Tightens Ties; Sanae Takaichi’s “High-EQ” Diplomacy. Bessent Urges Japan to Hike Rates, Meets Cautious Response. Behind the U.S.–Japan Alliance: New Balances and Bargaining

Trump’s first meeting with Japan’s new prime minister, Sanae Takaichi, began with Abe’s golf clubs and a baseball game, followed by a joint appearance on a U.S. Navy aircraft carrier in Yokosuka. Takaichi’s body language—linking arms, animated delight—projected warmth. This “high emotional intelligence” diplomacy prompted Trump to say: “From everything I’ve learned from Shinzo Abe and others, you will be one of the great prime ministers.” Still, this carefully crafted personal rapport was meant to pave the way for substantive talks.

(Image from the internet)

(Image from the internet)

Trump and Takaichi’s “Gold-Tinted Diplomacy”: Stronger Alliance, Vague Agreements

Trump’s Japan stop was a key leg of his Asia tour and fit neatly into Takaichi’s early diplomatic schedule. The two interacted frequently—from a call even before Trump’s plane landed, to a formal summit in Tokyo, to their joint appearance at the Yokosuka U.S. base—sending a clear signal of alliance strengthening.

Political ties and personal chemistry: Takaichi understands Trump’s diplomatic style. In their call she stressed that “Japan is an important country for the U.S.’s China strategy and Indo-Pacific strategy,” and she actively pushed the “Free and Open Indo-Pacific” vision. Trump reciprocated—praising her as a future “great prime minister” and promising, “Whenever, whatever help you need—anything I can do for Japan—we will do.” This close personal interaction set a positive tone for substantive negotiations.

$550 billion in investment and fuzzy trade deals: The two sides signed documents on trade and critical minerals, confirming Japan’s commitment to fund $550 billion worth of U.S. projects. However, White House documents show the agreements remain “vague”: the trade paper merely “notes with satisfaction the swift and continued efforts” of both countries, and the critical-minerals pact lacks specifics. This ambiguity gives Takaichi room at home amid fiscal pressure, while also reflecting the need for further talks on implementation.

Concrete progress in defense cooperation: Even before Trump arrived, Takaichi pledged to pull forward the target of defense spending to 2% of GDP to before March 2026, two years ahead of schedule. This directly answers Trump’s call for allies to shoulder more defense costs and stands out as one of the most substantive outcomes of the visit.

Bessent’s “Rate-Hike Nudge”: U.S.–Japan Policy Differences Surface

While Trump and Takaichi projected unity, U.S. Treasury Secretary Bessent sent a very different signal on monetary policy, prompting market jitters and a swift Japanese response.

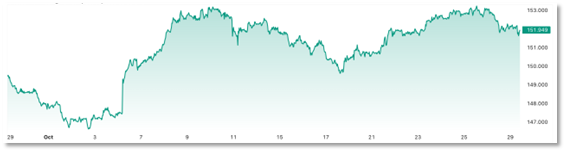

Rare public pressure from Bessent: After meeting Finance Minister Satsuki Katayama, Bessent used a U.S. Treasury statement to publicly urge Japan to adopt “prudent monetary policy” to anchor inflation expectations and prevent excessive FX volatility. He stressed that “the government’s willingness to allow the Bank of Japan policy space will be key,” read by markets as a warning against government interference with central-bank independence. The dollar promptly fell 0.3% against the yen to ¥151.59.

Japan’s quick downplay: Responding to Bessent’s remarks, Katayama moved quickly to cool things down. She said Bessent “may not have been urging the BOJ to raise rates,” and emphasized that he “is very familiar with the rules governing central banks.” The response signals Japan’s defense of monetary-policy independence—and its reluctance to see a rapid yen surge that could hurt export competitiveness.

Policy backdrop and deeper rift: Bessent’s stance isn’t new. As early as last August he said the BOJ was “behind the curve,” and his latest comments extend that line. Analysts believe Washington may be pursuing a weaker-dollar policy to support exports, pressuring Japan to allow yen appreciation. BOJ Governor Kazuo Ueda, however, insists on caution, citing U.S. growth slowing and Trump’s tariff policies as potential drags on Japan.

Japan Seeks Balance Between Alliance Politics and Economic Realities

The leaders’ political camaraderie and the treasurers’ policy divergence send mixed signals to markets and leave the BOJ facing tougher choices.

Market expectations vs. central-bank bind: Bessent’s comments lifted rate-hike expectations, yet markets broadly expect the BOJ to hold steady at its next meeting. Core inflation has stayed above the 2% target for more than three years, but real wages keep falling—a kind of “stagflationary pain.” Meanwhile, government debt stands at 235% of GDP; rate hikes could sharply raise debt-service costs.

The “Takaichi trade” and the yen dilemma: Since Takaichi won the LDP leadership, markets have bet on expansionary fiscal policy, producing the so-called “Takaichi trade”—buy stocks, sell yen. USD/JPY slid from 147 on October 3 into the 151 range. A weaker yen helps exporters but lifts import costs, stoking inflation and living-cost pressures.

Long-term policy path: The BOJ faces an “impossible trinity”:

Tighten faster and risk bond-market turmoil;

Stay loose and suffer yen depreciation and imported inflation;

Prioritize trade-friction responses and potentially sacrifice domestic recovery.

Most institutions think the BOJ can’t quickly exit “policy hibernation.” Its top priority has shifted from “fighting deflation” to “preventing crises.” Markets currently expect the next BOJ rate hike in December or January, but any follow-up steps will likely be very gradual.

As Trump and Takaichi raise glasses to a stronger alliance, the sparring between Bessent and Katayama exposes deeper contradictions in U.S.–Japan relations. Japan is striving to balance a fortified security alliance with monetary-policy autonomy—and the outcome will directly shape the recovery path of the world’s third-largest economy and the financial stability of the Asia-Pacific, and even the world.