Aave founder outlines plan to bring multi-trillion-dollar securities market onchain with V4

作者 Michael Ebiekutan

更新: 20 Jun 2026

熱門文章

Lending protocol Aave (AAVE) founder Stani Kulechov revealed a proposal to bring the multi-trillion-dollar securities market onto blockchain infrastructure, according to a blog post on Friday.

- Aave founder Stani Kulechov proposed bringing securities finance onchain through Aave V4, targeting repo, lending and tokenized collateral markets.

- The design leverages a hub-and-spoke liquidity model to improve capital efficiency while enabling risk-segmented financial markets.

- Kulechov argued that blockchain settlement could replace T+1 and T+2 settlement times with near-instant, atomic clearing and transparency.

Lending protocol Aave (AAVE) founder Stani Kulechov revealed a proposal to bring the multi-trillion-dollar securities market onto blockchain infrastructure, according to a blog post on Friday.

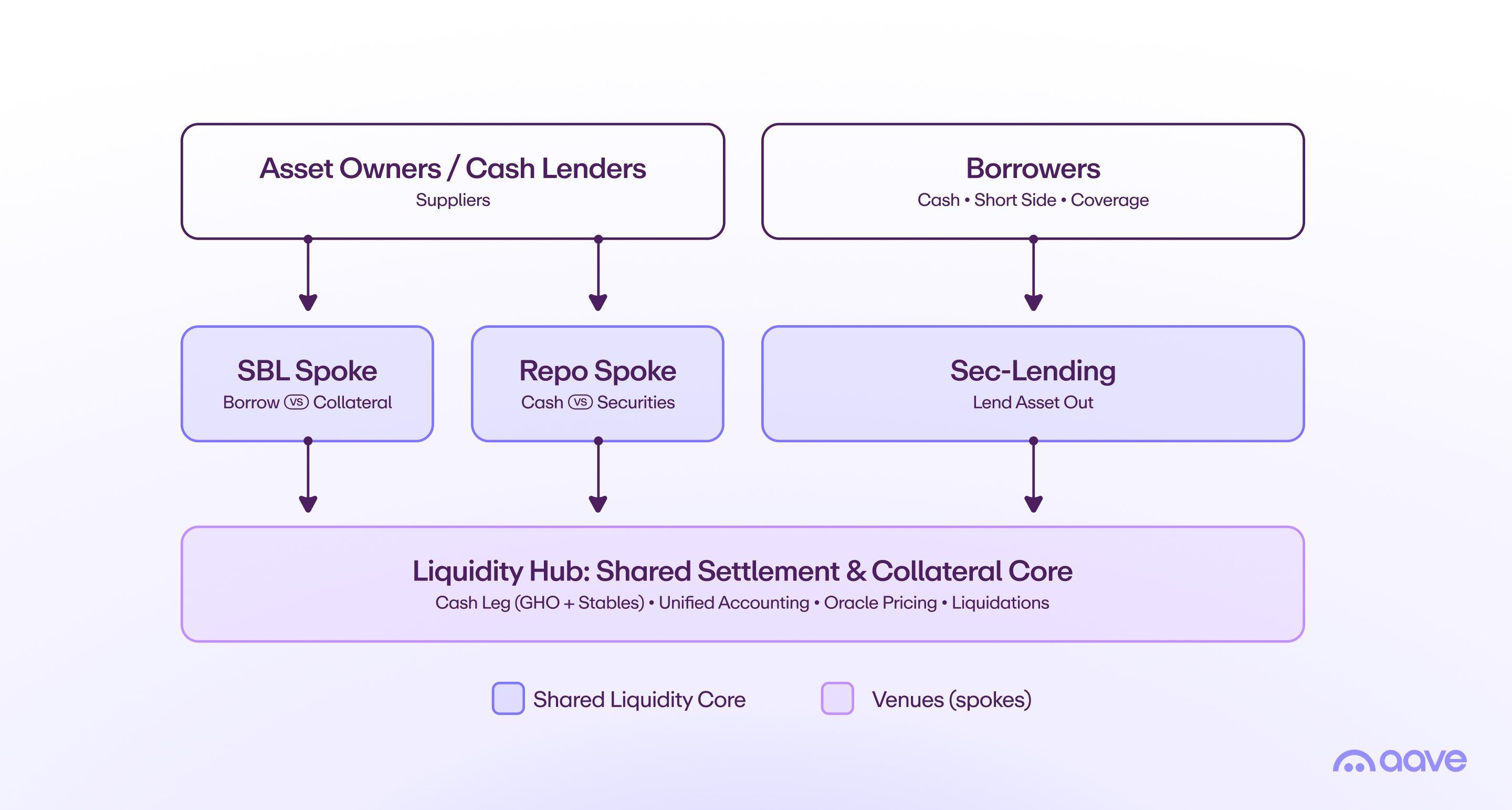

He argued that the protocol's V4 architecture could support tokenized securities-backed lending, repo markets and securities lending through a shared liquidity model.

Kulechov stated that securities finance remains one of the “largest markets that almost nobody outside Wall Street thinks about, and it is already starting to move onchain."

Aave to bring securities finance onto blockchain infrastructure

He noted that the US repo market averages $12.6 trillion in daily exposures, while margin lending stands at roughly $1.3 trillion. Kulechov further stated that securities lending currently accounts for approximately $4.6 trillion of assets, while wealth-management securities-backed loans exceed $400 billion.

Much of today's securities finance infrastructure relies on multiple intermediaries, including custodians, lending agents, prime brokers and clearing houses, creating higher costs, settlement delays and limited transparency. Kulechov argued that blockchain-based infrastructure could simplify those processes by making collateral management and settlement more efficient.

"The best way to move it onchain is to get the market structure right," Kulechov noted.

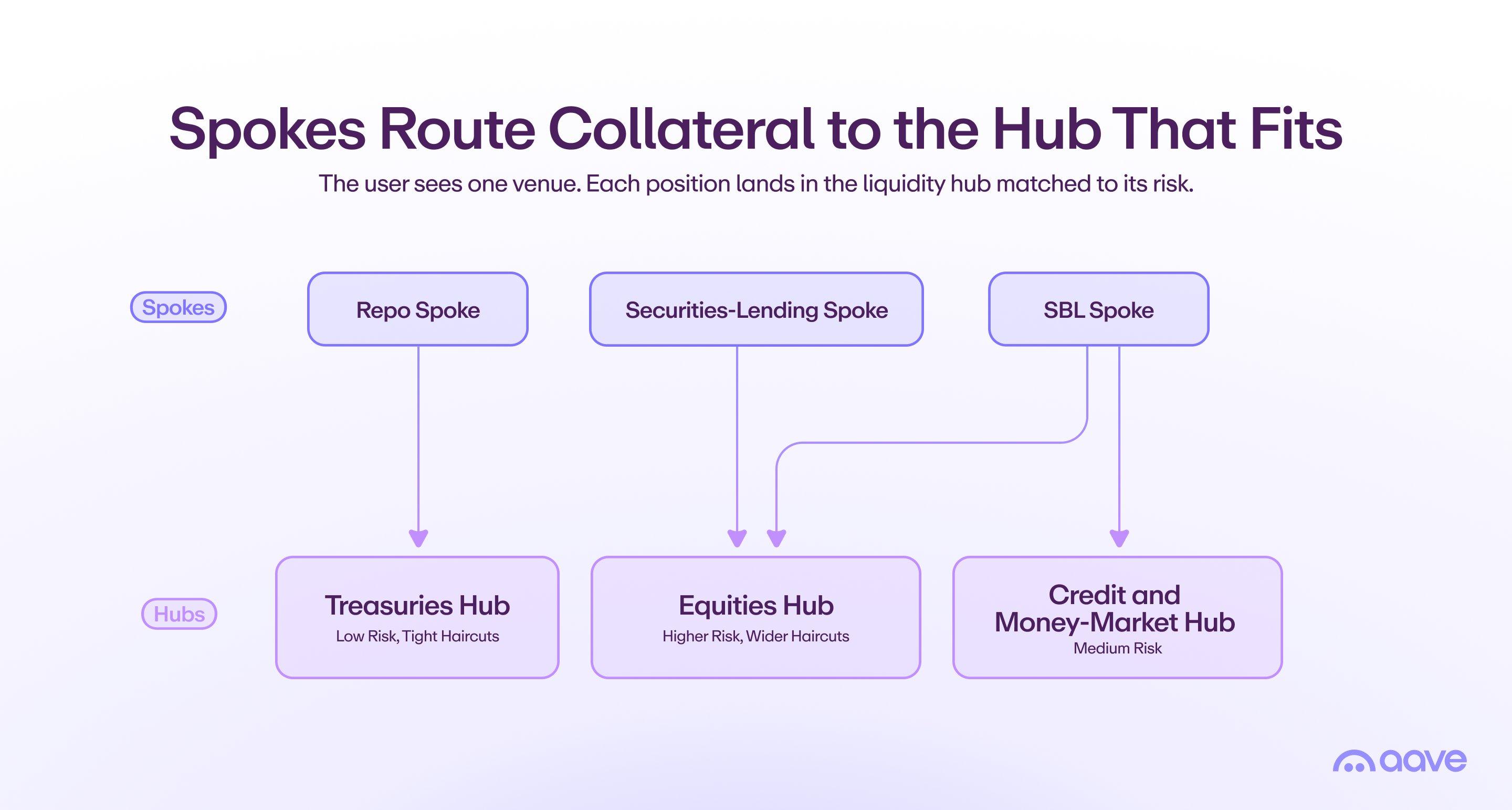

The proposal centers on Aave V4's hub-and-spoke architecture, where a central liquidity hub supplies capital to multiple specialized markets with independent risk parameters.

Kulechov noted that the design could accommodate several securities finance activities, including borrowing stablecoins against tokenized securities, conducting onchain repo transactions and lending tokenized securities to earn yield.

He suggested two possible market structures. One would rely on a single liquidity hub serving all markets, maximizing capital efficiency but concentrating risk.

The other would separate liquidity into multiple hubs based on asset classes and risk profiles. This allows Treasury-backed assets, credit products and equities to operate in isolated pools while remaining connected through shared market infrastructure.

"The practical path is a spectrum rather than a binary. Start unified for depth and simplicity, then graduate to category-and-risk hubs as collateral types scale and isolation becomes worth the fragmentation," Kulechov wrote.

Beyond technical design, Kulechov argued that blockchain infrastructure could reduce the role of traditional intermediaries, shifting functions such as collateral management, settlement and risk controls into protocol mechanisms. He stated that permissioned markets could still enforce regulatory requirements such as know-your-customer checks while accessing shared liquidity.

"A permissioned spoke or a jurisdiction-scoped hub enforces KYC, jurisdiction, and eligible-asset rules at the edge while still drawing on shared liquidity, so a regulated institution gets a venue that fits its rules without fragmenting the order book the rest of the market relies on,” Kulechov added.

Regarding settlement, Kulechov noted that traditional securities markets continue to rely on T+1 and T+2 settlement times. On the other hand, Aave V4 is designed to support atomic, continuous settlement and near-instant reconciliation onchain.

AAVE is trading at $73.2, up 0.2% over the past 24 hours and 13% in the past week at the time of publication.

超過一百萬用戶依賴 FXStreet 獲取即時市場數據、圖表工具、專家洞見與外匯新聞。其全面的經濟日曆與教育網路研討會協助交易者保持資訊領先、做出審慎決策。FXStreet 擁有約 60 人的團隊,分布於巴塞隆納總部及全球各地。

閱讀更多