[TMGM Financial Breakfast] Middle East Tensions and Rising Fed Rate Hike Expectations Deliver Double Blow — Could Gold Prices Continue to Pull Back?

Von Aiko Tanaka

Aktualisiert: 15 May 2026

BELIEBTE ARTIKEL

Spot gold weakened on Thursday as a stronger US dollar, elevated Treasury yields, and fading expectations for Federal Reserve rate cuts all weighed heavily on gold prices. Meanwhile, oil prices remained elevated due to ongoing Middle East conflict, keeping inflation pressures high, while the Beijing summit between Chinese and US leaders has become the market’s biggest variable.

The gold market currently lacks a clear directional catalyst, with price action showing a noticeably weak and volatile pattern.

The US Dollar Index rose 0.3% on Thursday, reaching a two-week high. This directly increased the holding cost of US dollar-denominated gold and created significant pressure on non-US investors.

At the same time, although US Treasury yields retreated slightly after earlier gains, they remain at relatively elevated levels overall. In particular, the 10-year Treasury yield previously approached its highest level in 11 months.

Together, these factors continue to create strong headwinds for non-yielding assets such as gold.

Expectations surrounding Federal Reserve monetary policy have also shifted significantly, further intensifying pressure on gold prices.

Driven by soaring energy prices linked to Middle East tensions, both the US Producer Price Index (PPI) and Consumer Price Index (CPI) recorded sharp increases in April, causing market expectations for Fed rate cuts to largely disappear.

According to the FedWatch tool, the probability of the Fed keeping rates unchanged through December has risen to 53.5%. The probability of cumulative rate cuts totaling 25 basis points has fallen to just 1.7%, while the probability of at least one 25-basis-point rate hike has climbed to 44.7%.

Although gold is traditionally viewed as an inflation hedge, rising interest-rate environments tend to weaken its attractiveness because the opportunity cost of holding gold increases significantly.

Geopolitical uncertainty remains the most important source of support for the gold market, while simultaneously representing a potential downside risk.

Tensions in the Middle East remain elevated, and the Strait of Hormuz is effectively under blockade, keeping oil prices at high levels.

Although Iranian state media reported that approximately 30 vessels had passed through the strait and some Chinese ships had been allowed to transit, reports of attacks and the broader blockade situation continue casting uncertainty over global energy supplies.

If the Middle East conflict fails to reach an effective resolution, gold may face downside pressure. However, shrinking inventories and tightening energy supplies could further fuel inflation, indirectly supporting gold prices.

High oil prices have already begun filtering into other goods and services, which is considered one of the key reasons recent US inflation data exceeded expectations.

At the same time, dissent within the Republican Party regarding the Iran conflict is also increasing. Although Congress has repeatedly rejected troop withdrawal resolutions, the number of Republican lawmakers supporting withdrawal has grown, signaling rising internal dissatisfaction.

This has further increased uncertainty surrounding the broader geopolitical situation.

Despite rising inflation pressures, recent US economic data has demonstrated notable resilience, helping support both the US dollar and risk assets.

US retail sales rose 0.5% in April, matching expectations. Consumers continued spending despite higher gasoline prices, suggesting that internal substitution effects remain limited.

Meanwhile, initial jobless claims rose slightly to 211,000 last week, while the overall labor market remains stable.

These economic indicators have strengthened market optimism toward the US economic outlook.

Market Analysis:

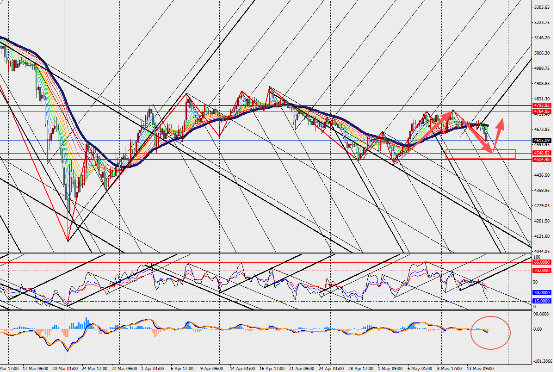

Gold continues to trend lower on the 4-hour chart timeframe, while both the MACD lines and histogram are expanding near the zero axis.

Investors should closely monitor the concrete outcomes of the China-US leaders’ summit, as well as actual shipping conditions through the Strait of Hormuz.

If Middle East tensions ease, gold could face further downside correction risks.

Conversely, if the energy crisis deepens or diplomatic progress disappoints market expectations, gold’s safe-haven appeal may once again regain strong investor support.

Aiko Tanaka is our precious metals specialist with 10 years of experience in commodity markets. She holds a degree in Geology and professional certification in Commodity Market Analysis, covering gold, silver, platinum, and palladium markets with mining industry insights. Alongside her analysis, Aiko has authored thought-leadership pieces on commodities and contributes educational content aimed at new investors in the sector.

Weiterlesen