Gold Rebounds in V-Shape After Sharp Selloff — Can Trump’s Ceasefire Talks Turn the Tide?

The sharp volatility in gold this week is deeply rooted in the rapidly evolving situation in the Middle East. The conflict between the United States and Iran has entered its fourth week, reshaping the regional landscape while sending shockwaves through global financial markets.

Geopolitical uncertainty is being transmitted into macro-financial conditions through three key variables — oil prices, inflation expectations, and interest rate trajectories — creating a complex and often conflicting impact on gold.

The Strait of Hormuz, a critical global energy artery, has effectively been disrupted, halting around one-fifth of global oil and liquefied natural gas shipments. This represents the most significant supply-side shock facing markets today. Although oil prices briefly plunged more than 10% on Monday following Trump’s remarks about potential talks, they rebounded on Tuesday as optimism over a quick resolution faded and news emerged of increased U.S. military deployments. Major institutions such as Goldman Sachs have already raised their oil price forecasts for 2026.

For gold, rising energy prices act as a double-edged sword. On one hand, persistent inflation pressures should support gold as a traditional hedge. On the other hand, the more critical impact lies in the repricing of central bank responses — particularly that of the Federal Reserve. If the conflict persists and energy prices continue to rise, this is not necessarily positive for gold. Supply-driven inflation could force central banks to maintain a tightening stance or even consider further rate hikes, thereby reducing the attractiveness of non-yielding assets like gold.

Market expectations for interest rates are shifting dramatically. Before the Middle East conflict escalated, markets widely expected two rate cuts this year. Now, investors have fully priced out rate cuts for the year and are even assigning more than a 30% probability of a rate hike before year-end. This hawkish shift is clearly reflected in the bond market: weak demand for a $69 billion two-year Treasury auction pushed yields sharply higher to around 3.944%, while the benchmark 10-year yield climbed above 4.419%.

At present, the gold market is in an extremely delicate and fragile position. In the short term, price direction is almost entirely dependent on the next developments in U.S.–Iran relations.

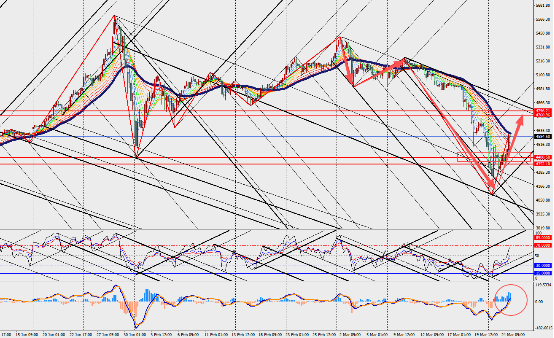

Market Interpretation:

On the four-hour chart, gold is showing a strong rebound, with MACD lines and volume bars expanding near the zero axis. In the second quarter, gold may face continued pressure. However, toward the end of the year, as inflation stabilizes and central banks gain more policy flexibility, the U.S. dollar may weaken and interest rates could decline, potentially restoring a more optimistic outlook for gold.