[TMGM Financial Breakfast] Cooling US PCE Data Sparks Gold Rebound, While a US-Iran Agreement Remains the Key Variable

Von Aiko Tanaka

Aktualisiert: 29 May 2026

BELIEBTE ARTIKEL

Gold is currently at a delicate crossroads where multiple narratives are converging. Softer PCE data and signs of broader economic cooling have provided short-term support, but the ultimate direction of gold will depend on the pace of geopolitical developments and the market’s repricing of Federal Reserve policy expectations.

The key catalyst behind the latest rebound in gold was the Federal Reserve’s preferred inflation gauge — the Core Personal Consumption Expenditures (PCE) Price Index. The April Core PCE data released on May 28 showed a month-on-month increase of just 0.2%, noticeably below the market expectation of 0.3% and significantly lower than the previous reading of 0.4%. The report provided a welcome sense of relief to financial markets.

Previously, geopolitical military tensions between the United States and Iran had fueled concerns over the Strait of Hormuz, sending oil prices sharply higher and leading markets to broadly expect another wave of energy-driven inflation. However, the softer-than-expected PCE report delivered a positive surprise. Inflationary pressures may not be as severe as previously feared. The immediate impact was a decline in the US Dollar Index, stronger Treasury prices, and renewed investor interest in non-yielding assets such as gold. Historically, whenever Core PCE comes in below expectations, market expectations for future Fed rate cuts tend to strengthen, benefiting gold prices. This time was no exception.

PCE was not the only supportive factor. Several economic reports released simultaneously helped build a broader fundamental case for gold’s rebound.

The second estimate of first-quarter GDP showed further economic moderation. The US Department of Commerce revised Q1 2026 GDP growth down from the initial estimate of 2.0% to 1.6%, below broad market expectations. The revision reflected slower private inventory investment and softer consumer spending. Weaker-than-expected economic growth suggests there may be less need for the Federal Reserve to maintain high interest rates, leaving more room for rate-cut expectations and providing support for gold.

Weekly initial jobless claims also increased during the same period. The signs of cooling labor market conditions further reinforced expectations that the Federal Reserve may eventually shift its policy stance. April durable goods orders showed modest fluctuations, while concerns about manufacturing activity generally increased. This added further support to the broader narrative of slowing economic growth.

Following the release of these reports, the US Dollar Index came under pressure and moved lower. Given the well-established inverse relationship between gold and the dollar, a weaker dollar naturally provided additional support for gold prices.

Taken together, these economic indicators point toward a relatively clear conclusion: the economy is cooling, while inflation may be proving less aggressive than previously feared. This has provided gold bulls with a rare opportunity to regain momentum.

Market Analysis:

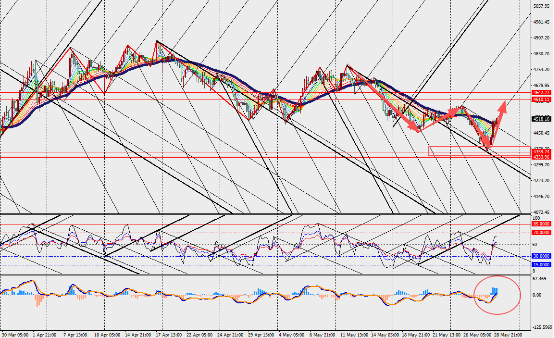

Gold rallied sharply on the 4-hour chart timeframe, while both the MACD lines and histogram expanded near the zero axis. Gold is currently sitting at a delicate intersection of multiple competing narratives. PCE data and broader signs of economic cooling have provided meaningful short-term support. However, the ultimate driver of gold’s next move will be determined by two key factors: the pace of geopolitical developments and the repricing of Federal Reserve policy expectations.

Aiko Tanaka is our precious metals specialist with 10 years of experience in commodity markets. She holds a degree in Geology and professional certification in Commodity Market Analysis, covering gold, silver, platinum, and palladium markets with mining industry insights. Alongside her analysis, Aiko has authored thought-leadership pieces on commodities and contributes educational content aimed at new investors in the sector.

Weiterlesen