U.S.–Iran Talks Collapse Again, Oil Prices Surge, Gold Gaps Lower as Markets Focus on U.S. CPI Data This Week!

News that the United States and Iran failed to reach an agreement on a peace proposal hit markets like a bombshell, directly igniting the energy market while severely damaging gold’s safe-haven sentiment. On the surface, this appears to be an asset seesaw effect triggered by geopolitical conflict, but beneath it lies a deeper three-way battle involving global inflation expectations, the direction of the U.S. dollar, and Federal Reserve policy expectations.

The core of the current situation lies in the continued tension surrounding the Strait of Hormuz. Although Qatari oil tankers and Panamanian bulk carriers were able to pass through with Iranian approval, U.S. Central Command clearly stated that more than 20 U.S. warships are now participating in maritime blockade operations against Iran, forcing 61 commercial vessels to reroute while leaving four ships unable to navigate. This hardline posture rapidly intensified market concerns over global crude oil supply disruptions.

Iran’s position remains equally firm. Tehran stated that it would never compromise simply to satisfy the United States. Trump sharply criticized Iran’s response on social media as “totally unacceptable” and rejected Iran’s core demands, including war compensation, sanctions relief, ending the blockade, and recognition of Iran’s sovereignty over the Strait of Hormuz. The enormous gap between the two sides has made hopes for a near-term ceasefire increasingly remote.

As Trump prepares for an upcoming visit to China, external pressure to end the Middle East conflict has intensified significantly. At the same time, hostile drones continue to appear over multiple Gulf states, while clashes between Israel and Hezbollah remain unresolved. Together, these developments suggest that geopolitical risks have not disappeared but have instead entered a new stage of prolonged confrontation.

Gold had rallied last week on optimism surrounding potential U.S.–Iran negotiations, once briefly holding above the $4,700 level. However, after the situation reversed on Monday, gold quickly gapped lower. This “expectation up, reality down” price action highlights how gold is currently behaving more like a risk asset than a traditional safe haven.

Higher oil prices directly push up global inflation expectations. Rising energy costs feed through into transportation, manufacturing, and other sectors, strengthening concerns that the Federal Reserve may maintain high interest rates for longer or delay rate cuts further. As a result, the U.S. dollar received support, while non-yielding gold faced increased holding-cost pressure. In addition, stronger-than-expected U.S. April nonfarm payroll data reinforced the resilience of the labor market, reducing the likelihood of aggressive Fed easing this year.

The upcoming U.S. April CPI and PPI data will become the main market focus this week. If CPI comes in below 3.0%, the dollar could weaken and gold may rebound. However, if CPI remains hot, markets may further strengthen expectations for a hawkish Federal Reserve, potentially pushing gold lower.

Market Interpretation

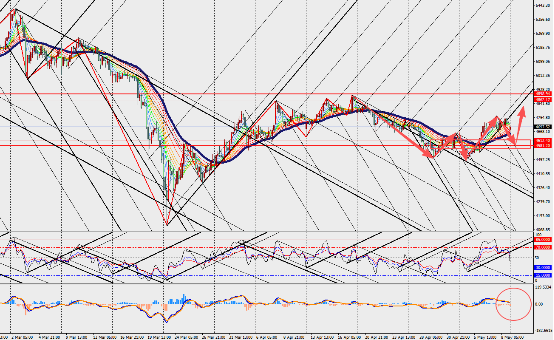

On the four-hour chart, gold has gapped lower and pulled back sharply, while MACD lines and volume bars continue expanding near the zero axis. The latest decline in gold reflects a combination of reversing geopolitical expectations and stronger macroeconomic data.

Investors should closely monitor this week’s U.S. inflation data, future statements from both the U.S. and Iran, and potential diplomatic developments during Trump’s China visit. For the gold market, short-term volatility is intensifying, but the medium- to long-term bullish framework remains intact.