Gold Crashes to Seven-Week Low! Double Blow From Middle East Conflict and Rising Inflation — Is the Gold Bull Market Suddenly Over?

By Aiko Tanaka

Updated: 20 May 2026

POPULAR ARTICLES

On May 19, gold prices plunged more than 1.8%. As the US-Iran conflict in the Middle East pushed oil prices above US$110, inflation concerns intensified while US Treasury yields climbed to fresh cyclical highs, sharply increasing the opportunity cost of holding gold amid elevated real interest rates.

Although gold has historically been viewed as an inflation hedge, under the current unique macroeconomic and geopolitical backdrop, it is facing unprecedented opportunity-cost pressure.

A stronger US dollar, surging Treasury yields, and elevated energy prices driven by Middle East tensions are collectively creating a perfect storm for gold prices.

This latest decline not only erased part of gold’s recent gains, but also highlighted the metal’s vulnerability in an environment where high interest rates and geopolitical risks are colliding.

Tuesday’s sharp selloff in gold was not an isolated event, but rather the direct result of multiple macroeconomic pressures erupting simultaneously.

The broad rise in global real interest rates remains the primary source of pressure on gold, while the strengthening US dollar has further intensified the negative environment.

The 10-year US Treasury yield climbed as high as 4.687%, reaching its highest level since January 2025.

Meanwhile, the 30-year Treasury yield surged to 5.197%, marking a fresh 19-year high.

The sharp rise in long-end Treasury yields directly increases the opportunity cost of holding non-yielding assets such as gold.

When investors can earn higher real returns from government bonds, the attractiveness of gold naturally weakens.

At the same time, the US Dollar Index rose 0.34% to 99.30, reaching a six-week high.

Gold priced in US dollars becomes more expensive for holders of non-US currencies, further suppressing physical demand and investment buying.

The key driver behind rising Treasury yields and dollar strength is growing market concern that inflation may once again spiral out of control.

And the source of those inflation fears points directly to the energy market disruptions caused by geopolitical conflict in the Middle East.

The conflict involving Iran, the US, and Israel has now lasted nearly three months, while Iran has effectively blocked the Strait of Hormuz.

Even though ceasefire agreements remain loosely intact, drone attacks targeting Gulf state infrastructure continue to occur frequently.

Last weekend’s attack on the UAE’s Barakah nuclear power plant further highlighted the risk of escalating tensions.

Elevated fuel costs are rapidly feeding through global supply chains, increasing core inflationary pressures worldwide.

As a result, central banks are being forced to maintain higher interest rates and may even face the possibility of further tightening later on.

This creates a double blow for gold:

On one hand, higher interest rates suppress gold’s safe-haven premium.

On the other hand, gold’s traditional inflation-hedging appeal is temporarily being overshadowed by the reality that central banks must first control inflation through tighter monetary policy.

Investors are now closely awaiting the release of the Federal Reserve’s April policy meeting minutes on Wednesday.

Current market pricing shows a 94.2% probability that the Fed will leave rates unchanged in June.

New Fed Chair Kevin Warsh faces an especially difficult challenge, as bond markets are demanding that he demonstrate a strong commitment to fighting inflation.

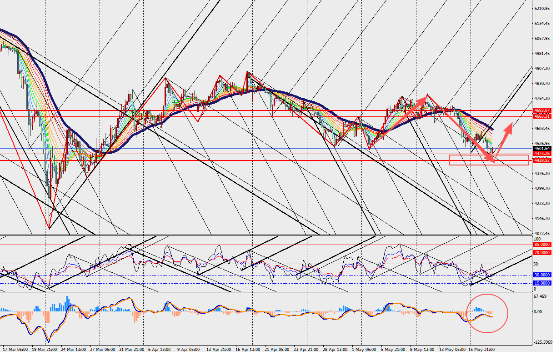

Market Analysis:

Gold declined again on the 4-hour chart timeframe, while both the MACD lines and histogram are showing converging bullish divergence near the lows.

Overall, the current gold selloff reflects the combined impact of tightening macroeconomic expectations, inflation transmission caused by geopolitical conflict, and ongoing US dollar strength.

In the short term, as long as oil prices remain elevated and Treasury yields continue fluctuating at high levels, gold prices are likely to remain under sustained correction pressure.

However, from a medium- to long-term perspective, gold has not yet lost the fundamental foundation of its broader bull market.

Aiko Tanaka is our precious metals specialist with 10 years of experience in commodity markets. She holds a degree in Geology and professional certification in Commodity Market Analysis, covering gold, silver, platinum, and palladium markets with mining industry insights. Alongside her analysis, Aiko has authored thought-leadership pieces on commodities and contributes educational content aimed at new investors in the sector.

Read More