[TMGM Financial Breakfast] The Gold Bull Market Is Only Halfway Through, with October Targeting Six Thousand Seven Hundred Fifty

By Aiko Tanaka

Date Published: 26 Feb 2026 | Date Modified: 26 Feb 2026

POPULAR ARTICLES

The global precious metals market remains red-hot. The current gold bull cycle is far from over. Based on historical cycle analysis, gold prices could climb to around six thousand seven hundred fifty by October 2026, around the time of the U.S. midterm elections.

On Thursday, spot gold moved higher in choppy trading, hovering near $5,185, as some investors began to question whether the rally’s long-term momentum might be fading.

Looking back at the five major gold bull cycles over the past fifty years, the current upswing has lasted only thirty-nine months, with prices gaining more than 200% while the U.S. dollar index declined by 13% over the same period. Overall, this performance aligns with the typical characteristics of a mid-cycle expansion. If gold continues to follow the historical average duration and magnitude of previous cycles, it could reach approximately $6,750 per ounce by October, around the U.S. midterm elections.

Traditional support factors remain strong, including declining global interest rates, geopolitical instability, rising economic uncertainty, and a weaker dollar. However, this cycle also displays structural differences: gold has gradually broken away from its traditional negative correlation with real interest rates and is increasingly evolving into a comprehensive hedge against systemic financial risk.

The current macro environment reflects multiple profound shifts. Global fiscal fragility is greater than in previous cycles, with high debt levels and persistent deficits reinforcing fiscal dominance. Political polarization in the United States has deepened, and global wealth inequality continues to widen. Together, these factors strengthen gold’s safe-haven and strategic allocation appeal.

Central bank buying remains a core pillar of support. Emerging market central banks still have significant room to increase gold reserves. The combined gold holdings of the top twenty emerging market central banks total roughly 7,500 tons. To approach developed market levels, they would need to add approximately 22,000 tons, equivalent to about six years of global annual mine supply. Continued net purchases by central banks effectively raise the price floor for gold.

Investment demand is also becoming more diversified. Beyond central banks and institutional investors, retail participation is accelerating. Physical gold sales through channels such as Costco remain robust, interest in gold-backed digital tokens is rising, and fractional ownership models are attracting more retail capital. Meanwhile, institutional allocations to gold remain relatively low, leaving room for future increases.

Market Interpretation:

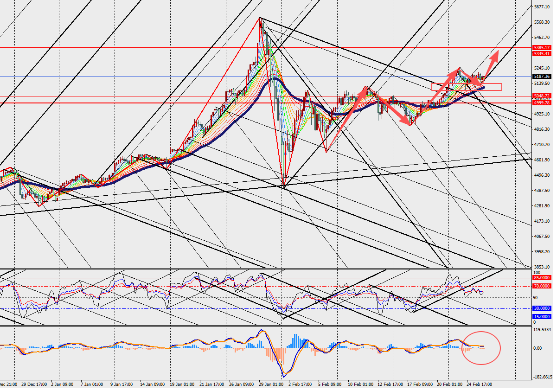

On the four-hour chart, gold is consolidating with a rebound bias, while MACD lines and histogram converge near the zero axis. Further dollar weakness would serve as an important catalyst for gold. The current dollar decline of 13% ranks as one of the mildest in historical comparison. If new catalysts emerge, the dollar could still face meaningful depreciation pressure.

However, a clear easing of geopolitical tensions, a dollar rebound, or a major shift in U.S. fiscal policy could exert significant downward pressure on gold prices.

Acuity Trading is a London-based fintech company founded in 2013 that specializes in AI-powered alternative data and sentiment analysis for trading and investments. They revolutionized the online trading experience by introducing visual news and sentiment tools, and today they continue to lead the fintech market with alpha-generating alternative data and highly engaging trading tools using the latest AI research and technology.

Read More