[TMGM Financial Breakfast] Has the Iran War Reinforced Gold’s Long-Term Bull Case? Saxo Bank Sees $10,000 by 2030

Ole Hansen, Head of Commodity Strategy at Saxo Bank, has released a major forward-looking view, stating that gold could theoretically reach $10,000 per ounce by around 2030. In his view, the impact of the Iran war is only a short-term market disturbance and will not interrupt the long-term bullish trend. Instead, structural positives such as rising stagflation risks, elevated global fiscal debt, and a weakening role of the U.S. dollar as a reserve currency are further reinforcing the foundation for gold’s upward movement.

Gold’s upside potential far exceeds that of most commodities. Even if prices were to double, overall physical demand — aside from jewelry — would not face any substantial impact. Hansen had originally expected gold to reach $6,000 within the year, but due to inflation pressures triggered by the Iran war and disruptions to the central bank rate-cut path, the realization of this target may be delayed by about six months.

The core logic supporting gold prices has not been shaken — in fact, it has been strengthened. Rising stagflation risks, growing fiscal debt concerns across countries, and increasing skepticism toward the long-term dominance of the U.S. dollar all continue to support gold. While the dollar’s global reserve currency status is unlikely to be fundamentally overturned in the short term, central banks and institutional investors across countries have formed a clear trend of reducing dependence on the dollar through asset diversification, with gold naturally benefiting as a safe-haven and reserve asset.

In the short term, rising inflation concerns have temporarily weakened gold’s upward momentum; however, over a longer horizon, once tensions ease, gold still has the potential to recover and reach new all-time highs. The fundamental drivers that initially pushed gold higher have not disappeared — in some cases, they have become even more favorable.

Regarding the $10,000 long-term target, Hansen emphasized that this is not a precise price forecast but rather a directional observation. The ability of gold to maintain demand at high price levels, combined with strengthening structural positives, makes this outlook realistically achievable.

Geopolitical conflict has fundamentally changed the macro environment for precious metals: before the war, the market was trading the narrative of fading rate-cut expectations and a weakening dollar; after the outbreak, surging energy prices, a stronger dollar, and delayed central bank easing expectations have taken center stage.

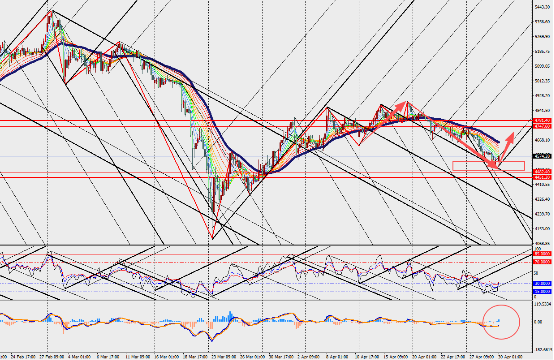

Market Interpretation:

On the four-hour chart, gold is showing a rebound after a decline, with MACD lines and volume bars expanding below the zero axis. The industry generally believes that the Iran war has only temporarily slowed gold’s upward trend and has not ended the bull market. Once geopolitical pressure in the Middle East gradually eases, gold is likely to experience a strong and rapid rebound.