[TMGM Financial Breakfast] Wells Fargo Sees Gold Surging to $8,000 as Currency Debasement Cycle Far from Over

Par Aiko Tanaka

Mis à jour: 17 Apr 2026

ARTICLES POPULAIRES

Wells Fargo Securities forecasts that gold could rise to $8,000 per ounce by 2027, driven by a global currency debasement trend. This implies a potential upside of about 66% from current levels near $4,800.

Wells Fargo presents a bullish scenario in which gold could surge significantly following its recent correction. After last month’s pullback, the bank believes the precious metal has the potential to rally sharply in the coming years.

Before the outbreak of the U.S.–Iran conflict on February 28, gold had been one of the strongest-performing momentum assets of the year. However, following the start of the war, prices declined. In March, gold futures fell nearly 11%, marking the largest monthly drop since June 2013.

Despite this setback, Wells Fargo expects the ongoing “currency debasement trade” — where central banks diversify away from fiat currencies such as the U.S. dollar and increase allocations to neutral reserve assets like gold — to drive prices significantly higher. The market is currently in the fourth global currency debasement cycle, which began in 2022.

Following the recent correction, gold prices are now closer to what Wells Fargo considers a fair value of around $4,500 per ounce. Looking ahead, continued currency debasement could push gold toward $8,000 per ounce by 2027. With spot and futures prices currently near $4,800, this suggests a potential upside of more than 66%.

On the downside, the bank outlines a bearish scenario in which gold could fall to $4,000 per ounce by the end of 2027, representing a decline of about 17% from current levels.

Wells Fargo uses the M2-to-gold ratio — the ratio of money supply to gold price — to identify currency cycles. According to this framework, the current debasement cycle began in 2022, driven by geopolitical events such as the Russia–Ukraine conflict and the U.S. rate-hiking cycle, which encouraged central banks worldwide to increase gold purchases.

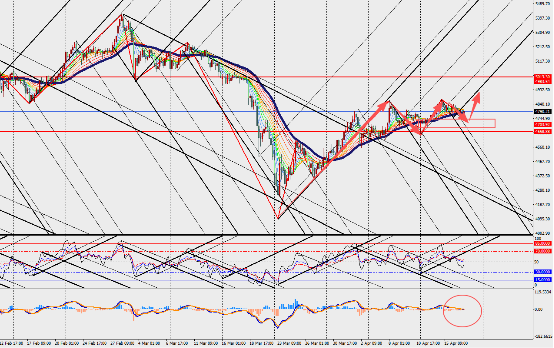

Market Interpretation:

On the four-hour chart, gold is trading sideways, with MACD lines and volume bars converging near the zero axis. Historically, major currency debasement cycles have occurred during periods such as the Great Depression, the Nixon era when the dollar was decoupled from gold, the early 21st-century war period, and the global financial crisis.

On average, these cycles have lasted about 8.5 years. The current cycle has been underway for approximately 3.5 years, suggesting it may still be far from its midpoint.

Aiko Tanaka is our precious metals specialist with 10 years of experience in commodity markets. She holds a degree in Geology and professional certification in Commodity Market Analysis, covering gold, silver, platinum, and palladium markets with mining industry insights. Alongside her analysis, Aiko has authored thought-leadership pieces on commodities and contributes educational content aimed at new investors in the sector.

Lire la suite