[TMGM Financial Breakfast] U.S.-Iran Airstrikes Intensify, Gold Faces Safe-Haven Paradox, U.S. CPI Test Ahead This Week!

Last Friday, gold staged a dramatic V-shaped reversal. U.S. February nonfarm payrolls unexpectedly fell by 92,000 jobs, far worse than the market expectation of a 59,000 increase, while the unemployment rate rose to 4.4%. The shockingly weak data immediately fueled market expectations that the Federal Reserve may accelerate interest rate cuts.

However, the combined pressure of a strong dollar and escalating tensions in the Middle East ultimately dragged gold lower. In early Monday trading, prices continued to weaken, at one point dropping more than 2% and falling below the $5,100 level.

Data released last Friday by the U.S. Bureau of Labor Statistics could be described as a “black swan” event. Private sector employment not only failed to grow but contracted sharply by 92,000 jobs, while January’s figure was revised down to just 126,000 job gains. More concerning, wage levels continued to rise, directly igniting discussions of stagflation risk — slowing economic growth accompanied by persistent inflationary pressure.

Following the data release, market expectations for Federal Reserve policy shifted rapidly. According to CME FedWatch, expectations for the first rate cut moved forward from October to July, while the probability of a September rate cut surged to 76%. U.S. interest rate futures now price in a total of 44 basis points of rate cuts this year, up from 39 basis points prior to the report.

Weak employment data would normally support gold, as a lower interest rate environment significantly reduces the opportunity cost of holding the non-yielding asset. Gold has historically been viewed as a long-term hedge against inflation. However, the reality proved more complicated: although the U.S. Dollar Index dipped 0.2% on Friday, it still recorded its largest weekly gain since November 2024, approaching a three-month high. This made dollar-denominated gold more expensive for overseas buyers, preventing prices from holding weekly gains.

While employment data stirred markets, geopolitical risks in the Middle East escalated sharply to a new level. Israel ordered a full evacuation of southern Beirut before launching heavy airstrikes, and over the weekend conducted precision strikes on Iranian oil and gas facilities. Oil prices surged overnight, breaking above $100 per barrel and pointing toward $120. This unprecedented move marked a significant escalation in joint U.S.-Israel military actions against Iran.

Gold’s long-term bull market logic remains intact, particularly during low interest rate cycles. Although global central bank gold purchases slowed in January, the monetary factors that have driven gold higher in recent years — long-term dollar depreciation trends, expanding global debt, and persistent geopolitical uncertainty — continue to develop.

Market Analysis:

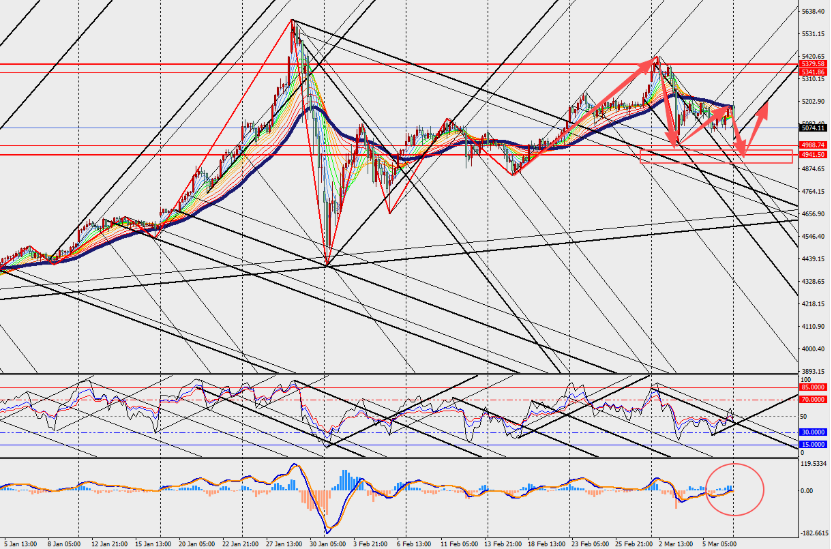

On the 4-hour chart, gold is consolidating with a downward bias, with MACD lines and histogram contracting near the zero axis. Geopolitical events typically impact prices only in the short term, while long-term monetary factors will once again dominate the trend. Gold continues to serve as a core stabilizing asset, with other assets fluctuating around it, and its long-term trajectory remains steadily upward. Overall, the market is awaiting upcoming heavyweight data releases such as CPI, retail sales, and GDP to provide clearer direction.