Intel Rides US Onshoring and AI Boom as Shares Extend Their Rally

Par Michael Rodriguez

Date de publication: 19 Jan 2026 | Date de modification: 19 Jan 2026

ARTICLES POPULAIRES

Intel is scheduled to report its fourth-quarter earnings after the close on 22 January, and investors will be watching closely for signs of an earnings turnaround.

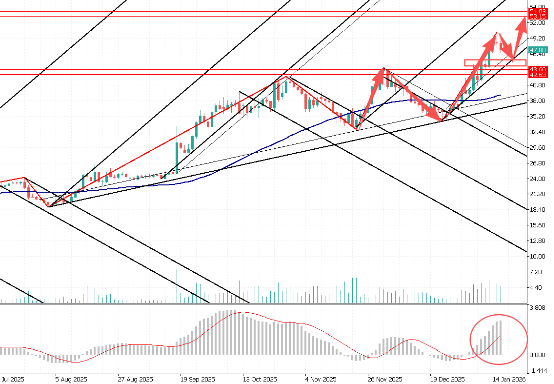

Intel’s sharp share-price gains at the start of the year suggest investors are increasingly optimistic that the chipmaker will win new foundry customers, paving the way for a meaningful return to the AI arena. After surging 84% in 2025, the stock is up a further 31% so far in early 2026. It is now trading near a two-year high, a striking reversal from the roughly 60% decline seen in 2024, when Intel appeared to be lagging competitors that were capitalising on the AI boom.

A series of catalysts has fuelled this renewed optimism: an improving financial outlook, fresh confidence reflected in recent analyst upgrades on Wall Street, speculation about new foundry customers, and enthusiasm over Intel’s potential to benefit from former President Trump’s “America First” industrial push.

Citi, KeyBanc and others have recently raised their ratings on the stock, citing robust end-market demand, progress in the foundry business, and the possibility of a deal with Apple that would see Intel chips used in future Macs and iPhones.

Manufacturing chips for AI and other compute workloads is a massive business opportunity, and progress on Intel’s 18A process technology could allow it to overtake Samsung and become the world’s second-largest contract foundry.

Citi analysts believe Intel stands to benefit from capacity bottlenecks in TSMC’s advanced packaging operations and, with support from the US government, is entering a unique window of opportunity to attract new wafer-fab customers.

Intel is also enjoying solid demand for its central processing unit (CPU) chips used in PCs and data centres. Even with GPUs supplied by Nvidia and other semiconductor makers doing the heavy lifting for AI workloads, CPUs remain indispensable in these systems, providing another tailwind for Intel.

As one of the few major chip manufacturers headquartered in the United States, Intel’s strategic position may also be boosting its share price, amid growing concern that geopolitical tensions could disrupt operations at TSMC, the world’s most critical contract chipmaker.

Market Commentary:

For Intel investors, the next major catalyst is likely to be next week’s earnings release. Consensus forecasts currently point to a 1% decline in revenue for 2025, followed by a 3% rebound in 2026. That means the real focus will be on the outlook: how CEO Pat Gelsinger and other Intel executives frame the company’s forward guidance and execution roadmap will be key to determining whether the recent rally still has further room to run.

Plus d’un million d’utilisateurs se tournent vers FXStreet pour des données de marché en temps réel, des outils de graphiques, des analyses d’experts et des actualités Forex. Leur calendrier économique complet et leurs webinaires éducatifs aident les traders à rester informés et à prendre des décisions éclairées. FXStreet s’appuie sur une équipe d’environ 60 professionnels répartis entre le siège de Barcelone et diverses régions du monde.

Lire la suite