US Dollar Index Price Forecast: DXY slides to one-month lows, tests key SMA confluence

작성자 Vishal Chaturvedi

수정됨: 8 Apr 2026

인기 기사

The US Dollar Index (DXY), which tracks the Greenback’s value against a basket of six major currencies, comes under heavy selling pressure on Wednesday, sliding to one-month lows after the United States and Iran agreed to a two-week ceasefire deal.

- The US Dollar Index (DXY) drops to one-month lows as easing geopolitical tensions weaken safe-haven demand.

- A sharp pullback in Oil prices weighs on the Greenback, with US Treasury yields retreating as inflation concerns ease.

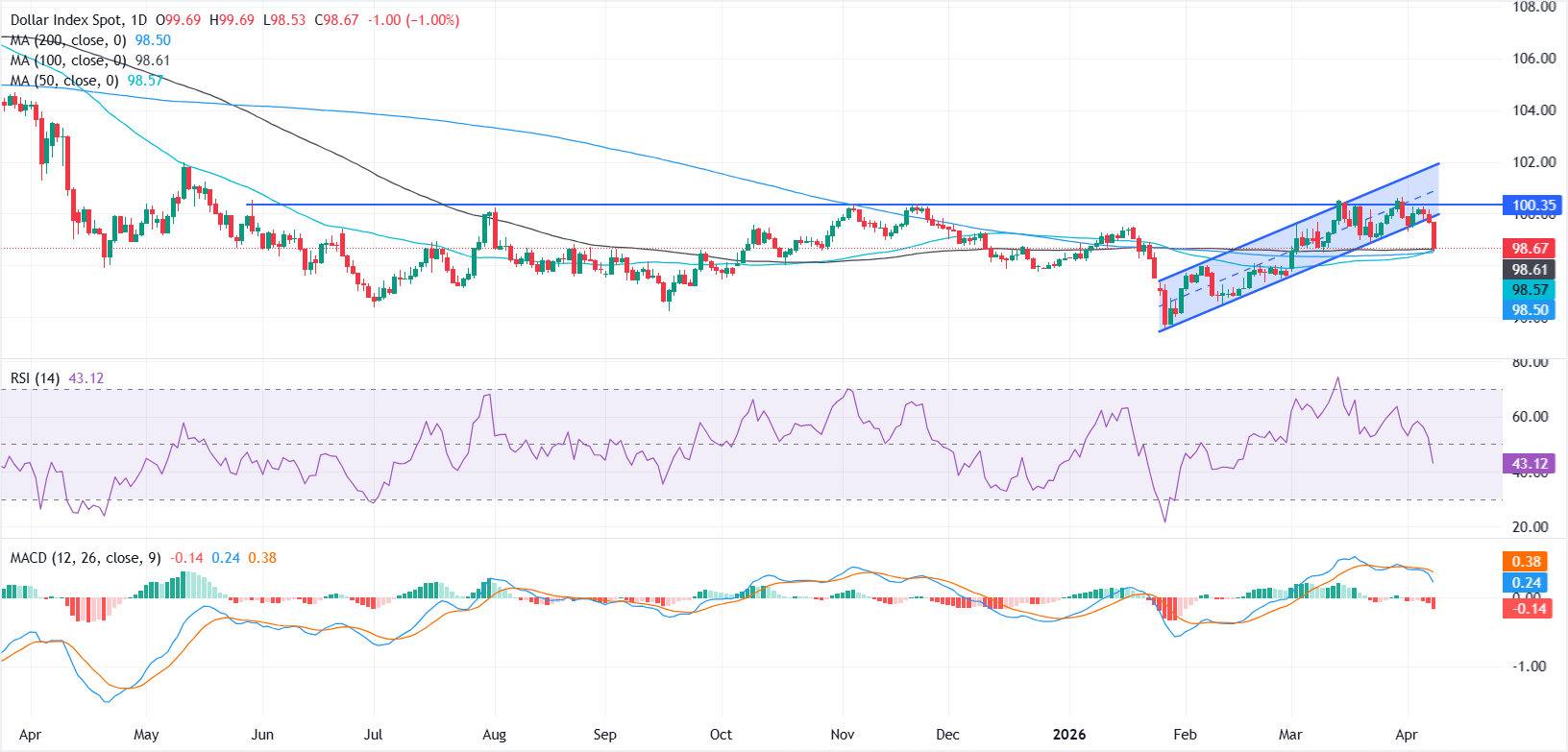

- Technically, DXY breaks below a rising channel and tests key support near 98.50-98.60, with momentum turning negative.

The US Dollar Index (DXY), which tracks the Greenback’s value against a basket of six major currencies, comes under heavy selling pressure on Wednesday, sliding to one-month lows after the United States and Iran agreed to a two-week ceasefire deal. At the time of writing, the DXY trades around 98.60, down nearly 1% on the day.

The US Dollar had been supported during the conflict as investors sought liquidity and safety, while surging Oil prices also boosted demand, as Oil is globally priced in USD. At the same time, Oil-driven inflation fueled expectations that the Federal Reserve (Fed) would keep interest rates higher for longer, lifting US Treasury yields and the Greenback.

Traders are now unwinding long US Dollar positions as the ceasefire reduces immediate geopolitical risks. Meanwhile, falling US Treasury yields are adding further downside pressure on the Greenback, as a sharp pullback in Oil prices eases inflation concerns and revives Fed rate cut expectations.

From a technical perspective, the US Dollar Index (DXY) has decisively broken below an upward-sloping parallel channel that had guided price action since late January, signaling a shift in near-term structure.

The move follows repeated failures to sustain gains above the 100.00–100.50 zone, a multi-month resistance area that has capped upside attempts since May 2025.

The latest leg lower now brings prices toward a key confluence support zone, where the 50-day, 100-day, and 200-day Simple Moving Averages (SMAs) have converged around the 98.50-98.60 region.

Holding above this area may offer some near-term stabilization, while a decisive break below could accelerate downside momentum and extend the broader downtrend.

On the upside, the 99.00 level acts as initial resistance, with a stronger barrier at the 100.00-100.50 zone. Rallies are likely to be capped unless there is a sustained move above this zone.

Momentum has also cooled, with the Relative Strength Index (14) slipping toward the low-40s and the Moving Average Convergence Divergence (MACD) turning negative, suggesting fading upside pressure.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

100만 명이 넘는 사용자가 FXStreet를 통해 실시간 시장 데이터, 차트 도구, 전문가 인사이트, 포렉스 뉴스를 이용합니다. 포괄적인 경제 캘린더와 교육 웨비나는 트레이더가 정보를 유지하고 신중한 결정을 내리도록 돕습니다. FXStreet는 바르셀로나 본사와 전 세계 지역에 걸쳐 약 60명의 팀으로 구성되어 있습니다.

더 읽기