Dow Jones Industrial Average toasts peak inflation, then drops the glass

Oleh Joshua Gibson

Dikemas kini: 15 Jul 2026

ARTIKEL POPULAR

The Dow Jones Industrial Average spent most of Wednesday rewarding the disinflation trade and the final two hours dismantling it.

- DJIA tested below 52,500 after surrendering a 370-point afternoon rally.

- June wholesale prices unexpectedly fell 0.3% MoM and the New York Fed president called the inflation peak, yet futures still price roughly 60% odds of higher rates by the end of October.

- Semiconductor names shed as much as 11% while three of the index's technology heavyweights rose about 3% apiece; Thursday's Retail Sales decide whether the fade has legs.

The Dow Jones Industrial Average spent most of Wednesday rewarding the disinflation trade and the final two hours dismantling it. A surprise negative June wholesale inflation print at 12:30 GMT set off a grind that stretched 370 points to a session high of 52,830, and a late unwind then handed every one of them back. The index trades near 52,500, down around 0.12% on the day.

Disinflation arrives with an asterisk

The June Producer Price Index (PPI) fell 0.3% MoM against a consensus for a flat reading, pulling the annual rate down to 5.5% from 6.0% and undershooting the 6.2% forecast. The core measure rose a softer-than-expected 0.2% MoM, landing one day after Tuesday's cooler Consumer Price Index (CPI) release had already prompted traders to scale back near-term tightening bets. The New York Federal Reserve president supplied the rhetorical garnish, arguing there are encouraging reasons to believe inflation has peaked and should edge lower over the coming quarters.

The awkward detail sits in the annual columns, where headline wholesale inflation at 5.5% and core at 4.7% both run at more than double the Fed's 2% target; the core rate even accelerated from the prior month's 4.6% while beating forecasts. Research desks canvassed after the release argued that single soft prints do not retire hike risk when the level remains this far from mandate, and that the tape is overreacting to one number at a time.

Autumn hikes refuse to leave the tape

Rate futures tell the same story in cleaner numbers: pricing for a move at this month's meeting has faded since Tuesday's CPI, yet markets still assign roughly 60% odds that the policy rate sits a quarter point or half point higher by the conclusion of the October meeting. The Fed Chair's 14:00 GMT congressional testimony came and went without dislodging that pricing.

The real economy keeps arguing the hawks' side of the ledger, with the July Empire State Manufacturing Index printing 15.6 against an 8.8 consensus and a 5.7 prior. The Beige Book and a run of Fed speakers round out a crowded docket, which gives the committee every opportunity to keep its options open into this month's decision.

The average dodges the shrapnel and bleeds anyway

Semiconductors supplied the session's carnage, and the sector managed the impressive trick of gapping higher premarket on a guidance raise from Dutch lithography monopolist ASML before unwinding the entire bid. Micron (MU) trades down 9%, SanDisk (SNDK) down more than 11%, Lam Research (LRCX) off more than 6%, with Intel (INTC), Advanced Micro Devices (AMD) and Marvell (MRVL) between 5% and 7% lower; the benchmark semiconductor basket sheds 4%.

The Dow Jones Industrial Average sidesteps nearly all of that by construction, since none of the names on the casualty list holds a seat among its 30 constituents, and three that do, Apple (AAPL), Microsoft (MSFT) and Amazon (AMZN), trade up roughly 3% apiece. An index that gets that kind of sponsorship from its technology bench and still sits red near the session low is an index whose other 27 members spent the day getting sold; the breadth message is uglier than the headline change suggests.

Hormuz keeps the inflation call honest

Crude Oil complicates the peak-inflation arithmetic from the supply side, with West Texas Intermediate (WTI) holding above $78 per barrel and Brent above $83 after Central Command confirmed a further round of strikes on Iranian targets. Tehran's attacks on commercial shipping around the Strait of Hormuz have kept last month's peace framework functionally suspended, and the war premium in the barrel is now a July problem layered on top of June's friendlier data.

That sequencing matters for anyone extending today's soft PPI into a policy call, because the wholesale disinflation on the tape predates the latest escalation almost entirely. Energy passthrough with a lag is precisely the sort of supply shock the committee has flagged while holding rates, and it argues for treating the morning's rally as a trade rather than a regime change.

Thursday hands the microphone to the consumer

Thursday's 12:30 GMT slate is the week's real referendum, headlined by June Retail Sales with consensus at 0.2% MoM after May's 0.9% surge, the control group seen at 0.5% after 0.7%, and the ex-autos measure expected at -0.1%. Initial Jobless Claims are seen near 217K, and the Philadelphia Fed survey is expected at 13 after 10.3, neither of which suggests a labour market forcing the committee's hand.

Friday adds the preliminary July Michigan Consumer Sentiment Index, seen at 51 after 49.5, along with the one-year inflation expectations series that printed 4.6% last month. A soft consumer feeds the peak-inflation narrative while quietly denting the earnings math; a hot control group re-arms the October hike pricing within 24 hours of today's celebration. Either outcome lands on a tape that has already shown how it treats good news.

Dow Jones Industrial Average technical levels

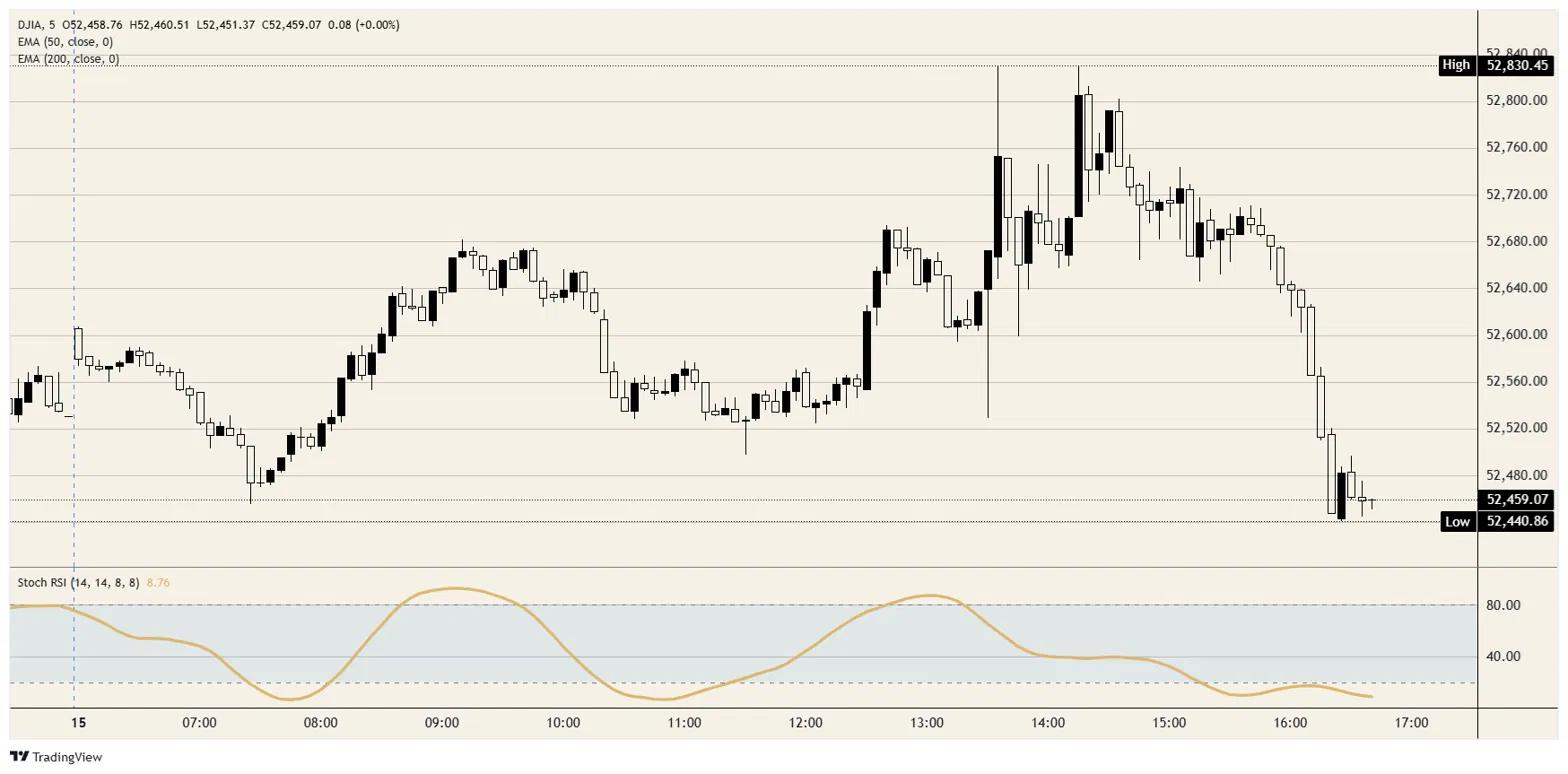

Resistance: The 52,700 shelf that gave way during the afternoon slide is the first hurdle, ahead of the rejected session high at 52,830. Beyond that, the 53,000 handle guards the early-July record zone, with the daily Stochastic Relative Strength Index curling down out of the overbought band at 69.

Support: Wednesday's low near 52,440 is the immediate floor, and the 52,000 handle sits behind it, the level that absorbed last week's washout and capped the late-June consolidation. The rising 50-day Exponential Moving Average near 51,280 is the last structural backstop before the picture changes character.

Bias: Bearish. A 370-point rejection from 52,830 on the day the disinflation case landed its best headline in months leaves sellers holding the tape into Thursday's Retail Sales; below 52,700 the path of least resistance points at the 52,000 handle. Only a daily close back above 52,830 repairs the structure and reopens the record zone.

Dow Jones 5-minute chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

Lebih sejuta pengguna bergantung pada FXStreet untuk data pasaran masa nyata, alat carta, pandangan pakar dan berita Forex. Kalendar ekonomi yang komprehensif dan webinar pendidikan mereka membantu pedagang kekal bermaklumat dan membuat keputusan yang dikira. FXStreet disokong oleh pasukan kira-kira 60 profesional di ibu pejabat Barcelona dan pelbagai wilayah global.

Baca Lagi