Why the New Zealand Dollar may not benefit from expected RBNZ rate hike

Oleh FXStreet Insights Team

Dikemas kini: 7 Jul 2026

ARTIKEL POPULAR

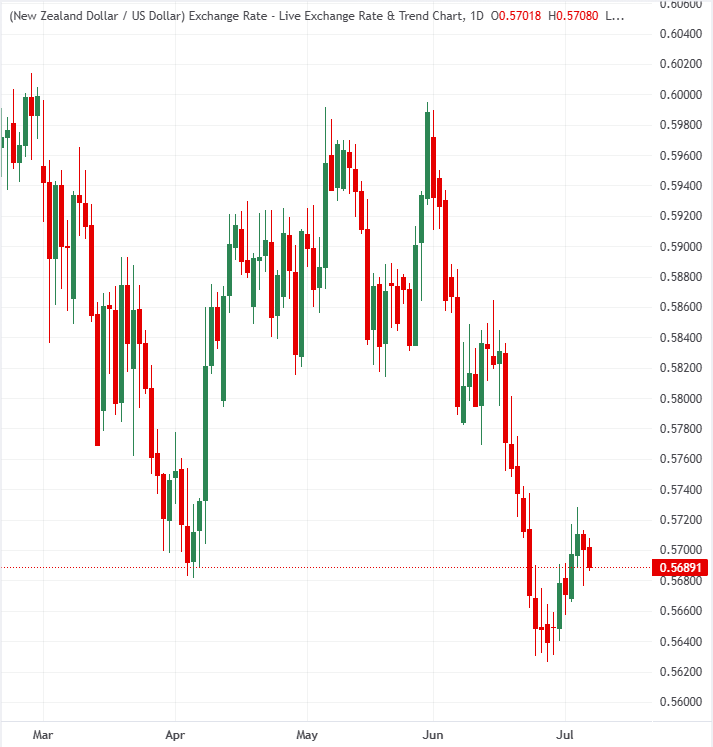

The New Zealand Dollar (NZD) continues to trade subdued against the US Dollar (USD) as markets brace for the Reserve Bank of New Zealand's (RBNZ) upcoming monetary policy decision.

The New Zealand Dollar (NZD) continues to trade subdued against the US Dollar (USD) as markets brace for the Reserve Bank of New Zealand's (RBNZ) upcoming monetary policy decision.

Following a rare 3-3 split vote at the central bank's previous meeting in May (where Governor Anna Breman had to cast a tie-breaking vote to keep the Official Cash Rate on hold at 2.25%), expectations are for a 25-basis-point interest rate increase to 2.50%.

While this tightening is meant to solidify the RBNZ's inflation-fighting credentials, a significant drop in global energy costs following a recent US-Iran diplomatic agreement has altered the long-term outlook. Because aggressive rate-hike paths are already heavily embedded in current market positioning, institutional analysts warn that the local currency faces limited appreciation potential and clear medium-term downside risks.

Extreme tightening bets cap the Kiwi's appreciation potential

Foreign exchange strategists at Rabobank highlight that while a near-term interest rate hike is expected by consensus, the broader trajectory of monetary policy priced into asset markets is overly ambitious.

With markets factoring in nearly four rate increases over the next year, any indication that the central bank is softening its tone due to a fragile domestic economic recovery or a substantial cooling in inflation pressures could trigger a sharp asset correction.

With so much tightening already in the price, we don’t see much scope for the NZD to improve its position on the G10 performance table this year. Indeed, any sign that the RBNZ is backing down on its hawkish tone could leave the NZD vulnerable.

Excessive market expectations set the stage for a medium-term drag

The macro research team at Commerzbank argues that while a near-term hike will send a clear signal of intent to combat stubborn price pressures, the structural horizon remains challenging for the Kiwi. They emphasize that current multi-hike market expectations are fundamentally out of touch with leading indicators that show inflation peaking, meaning the eventual unwinding of these aggressive assumptions will inevitably weigh on the currency.

We consider the market expectation of 3.5 hikes over the next 12 months to be excessive. Consequently, the pricing out of these hikes in the coming months is likely to weigh on the kiwi.

Banks anticipate limited strength for the New Zealand Dollar

The banks anticipate an ultimately downward-biased trajectory for the New Zealand Dollar, noting that its bullish momentum has run out of space. Rabobank projects that the currency will remain locked in choppy, range-bound territory against the US Dollar, given that its potential yield advantages are already fully accounted for by market participants.

Commerzbank underscores that while the expected upcoming RBNZ's rate decision may provide a fleeting knee-jerk burst of support, the structural necessity to price out excessive monetary tightening bets as inflation falls will act as a persistent macroeconomic drag on the Kiwi over the coming months.

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

Lebih sejuta pengguna bergantung pada FXStreet untuk data pasaran masa nyata, alat carta, pandangan pakar dan berita Forex. Kalendar ekonomi yang komprehensif dan webinar pendidikan mereka membantu pedagang kekal bermaklumat dan membuat keputusan yang dikira. FXStreet disokong oleh pasukan kira-kira 60 profesional di ibu pejabat Barcelona dan pelbagai wilayah global.

Baca Lagi