Yen Keeps Sliding While Japanese Stocks Party at Record Highs! Rate-Hike Pressure Surges and Policy Hits a “Takaichi Trade” Dilemma

Por Sarah Chen

Data de Publicação: 3 Nov 2025 | Data de Modificação: 18 Dec 2025

ARTIGOS POPULARES

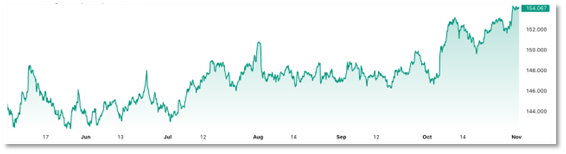

The yen has fallen to an eight-month low at 153.52, while the Nikkei 225 has broken through 51,000 to a record high—an ice-and-fire finale playing out in real time. As “Takaichi-nomics” sustains expectations for monetary easing, 96% of economists now expect the Bank of Japan to hike in Q4. Markets stand at a critical crossroads: a policy turn could end years of carry trades and potentially trigger chain reactions across global capital markets.

Yen weakness has extended to an eight-year low, the much-discussed “Takaichi trade” is in full swing, and economists’ expectations for a BOJ rate hike are heating up. Together, these dynamics hint that FX and equity markets may be heading for a new phase.

Origins of the Weaker Yen and the “Takaichi Trade”

USD/JPY recently slipped below the 153 handle, hitting an eight-month low. The core drivers are the market’s expectations for policies under the new Prime Minister, Sanae Takaichi, combined with the BOJ’s wait-and-see stance.

Policy divergence between the U.S. and Japan: On October 30, the BOJ kept its policy rate unchanged at 0.5%. While the Fed has also cut rates, its stance still leaves the U.S.–Japan rate gap wide—and even widening. Interest rates anchor currency pricing: when returns abroad far exceed those in Japan, global capital naturally sells yen and buys dollars, pushing the yen lower.

Rise of the “Takaichi trade”: Investors broadly expect Prime Minister Sanae Takaichi to continue a policy mix centered on accommodative monetary policy and active fiscal expansion—dubbed “Takaichi-nomics.” In markets, this has spawned the so-called “Takaichi trade”: sell the yen and buy Japanese equities, further exacerbating yen weakness.

Meet Japan’s “Fireball,” Takaichi Sanae, its polarising new leader

Imported inflation and a BOJ dilemma: Persistent yen depreciation heightens Japan’s imported-inflation risk. Core CPI rose 2.9% YoY in September, above the BOJ’s 2% target and accelerating. Yet with real wages still falling and household purchasing power under pressure, the BOJ faces a tough balance between supporting growth and controlling inflation.

Authorities’ Response and Market Expectations

Japan’s authorities have shown high alert as the yen drops rapidly.

Official warnings of intervention: Finance Minister Satsuki Katayama said authorities are watching FX moves with “a strong sense of urgency.” After the warning, the yen briefly firmed. The 155 level is viewed as a key psychological line; if the yen slides there too quickly, the likelihood of direct government intervention rises sharply.

A Q4 window for hikes: Although the BOJ stood pat in October, it has indicated a willingness to raise rates if the economy and inflation evolve as projected. Surveys show most economists expect a policy hike in Q4. The December meeting is the key checkpoint, and many expect a move to 0.75%. However, if Prime Minister Takaichi takes a cautious view of policy normalization, a delay is possible.

What to Watch Next

Traders should monitor the following signals to confirm market direction:

Clear guidance from the BOJ: Watch Governor Kazuo Ueda’s comments around the December meeting, especially on whether a virtuous wage–inflation cycle has formed.

Inflation verification: Keep a close eye on Tokyo core CPI, which has stayed above the 2% target for more than three and a half years—this is the BOJ’s most critical input.

Substance of “Takaichi-nomics”: Assess the scale, details, and execution of the new cabinet’s fiscal stimulus. This will determine the strength and durability of the “Takaichi trade.”

Global spillovers: The Fed’s rate path and the global growth outlook will influence U.S.–Japan rate differentials and risk sentiment, indirectly steering the yen and Japanese stocks.

How a Yen Rate Hike Could Hit Markets

All told, a BOJ hike would mainly impact U.S. equities via liquidity and valuations—and the market is already flashing some warning signs.

Liquidity and valuation shock: Some analysts argue that the normalization of Japanese policy could end a key liquidity source that has supported elevated U.S. equity valuations in recent years. Strategists have observed a tight relationship between Nasdaq valuations and Japan’s real bond yields. That implies rising real yields in Japan could directly pressure U.S. tech valuations.

History’s cautionary tale: Xu Xiaoqing of Dunhe Asset calls this risk a “gray rhino”—high-probability, high-impact, and widely recognized. He warns the BOJ may be forced to hike rapidly at some point in 2025 to fight inflation, delivering a major hit to global liquidity. Historically, when the short-term U.S.–Japan rate spread narrows below 400 bps, U.S. equities tend to struggle and volatility increases.

A BOJ rate hike hangs over U.S. stocks like a Damoclean sword—tightening global liquidity and pulling capital back home, posing a material threat to U.S. equities, especially richly valued tech names.

Mais de um milhão de usuários confiam na FXStreet para dados de mercado em tempo real, ferramentas de gráficos, insights de especialistas e notícias de Forex. Seu calendário econômico abrangente e webinars educacionais ajudam os traders a se manterem informados e tomarem decisões calculadas. A FXStreet conta com uma equipe de cerca de 60 profissionais, divididos entre a sede em Barcelona e diversas regiões globais.

Ler mais