[TMGM Financial Breakfast] U.S.–Iran Talks Stall as Gold Faces Pressure Ahead of Central Bank “Super Week”

While markets continue to monitor developments in the Middle East, attention is increasingly shifting toward this week’s major central bank decisions. In addition to the Federal Reserve, the European Central Bank, Bank of England, and Bank of Japan will all announce policy decisions. Key economic data, including U.S. first-quarter GDP and March PCE inflation, will also be released.

Iran has made it clear that it will not engage in negotiations until the U.S. lifts its blockade of Iranian ports, while Washington continues to leverage both military and economic pressure. This deep trust deficit has prolonged the blockade of the Strait of Hormuz, leaving around one-fifth of global oil shipments disrupted. Goldman Sachs has pushed back its timeline for a return to normal export levels from mid-May to late June and has significantly raised its fourth-quarter oil price forecast.

Under normal circumstances, escalating geopolitical tensions, rising oil prices, and increased safe-haven demand would provide strong support for gold. However, the current environment is different. The core issue is that persistently high oil prices are fueling a more concerning threat than the conflict itself — stubborn inflation.

Global investors are increasingly focused on the risk of inflation getting out of control. This is not demand-driven inflation, but rather cost-push inflation caused by disruptions in oil supply. While inflation typically supports gold by eroding currency purchasing power, excessive inflation expectations can shift central bank policy — turning into a negative factor for gold.

Markets are now repricing the Federal Reserve’s policy path. Just last Friday, futures markets suggested nearly a 40% probability of rate cuts by year-end. By Monday, following the surge in oil prices, expectations for potential rate hikes have edged higher. If the Fed maintains elevated rates — or even resumes tightening — to contain inflation, the opportunity cost of holding non-yielding gold will rise sharply.

At the same time, the prolonged U.S.–Iran standoff has inadvertently strengthened the U.S. dollar. For investors holding other currencies, a stronger dollar makes gold more expensive, reducing global demand.

Even if the conflict escalates further, it is unlikely to reach extreme levels. Markets are becoming increasingly desensitized to developments related to Iran. This does not mean investors are ignoring the situation, but rather that geopolitical risks are now being interpreted through an inflation-driven framework. In this context, gold is no longer the primary beneficiary.

Market Interpretation:

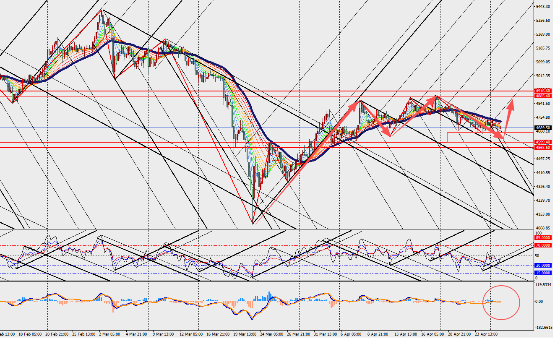

On the four-hour chart, gold remains range-bound, with MACD lines and volume bars converging near the zero axis. The market focus is shifting from geopolitical negotiations in Islamabad to central bank decisions.

This week’s cluster of policy meetings — including those of the Federal Reserve, Bank of Japan, European Central Bank, and Bank of England — will be critical in determining gold’s direction. If the Fed signals a more hawkish stance in response to rising inflation, gold could face deeper downside pressure.