[TMGM Financial Breakfast] Middle East War Risks Continue to Loom as Gold’s Mild Rebound Struggles Against Pressure From Oil and Bond Yields

Ni Aiko Tanaka

Na-update: 19 May 2026

Sikat na Artikulo

Spot gold edged slightly higher on a weaker US dollar, but surging oil prices and US Treasury yields hitting fresh cyclical highs created a double headwind that limited gold’s gains.

Markets continue to swing between fragile hopes for Iran peace negotiations and fears of potential supply disruptions, leaving investor sentiment highly sensitive.

This not only reflects gold’s complicated role as a traditional safe-haven asset, but also signals that precious metals could face heightened volatility in the near term.

The core logic behind current gold price movements remains deeply tied to the latest developments in the Middle East conflict.

On Monday, US President Donald Trump announced that he had paused planned military strikes against Iran after Tehran submitted a new peace proposal through Pakistan, allowing room for negotiations aimed at ending the US-Iran conflict.

The announcement itself carried some signs of de-escalation.

Trump mentioned that leaders from Qatar, Saudi Arabia, and the UAE had requested a temporary delay in military action, while also suggesting that a potential agreement could satisfy multiple parties.

However, Iran’s response remained firm.

Iran’s Supreme Joint Military Command issued a clear warning, stating that its armed forces were fully prepared to act at any moment.

Iran’s peace proposal reportedly focused on ending the conflict, reopening the Strait of Hormuz, easing certain sanctions, and unfreezing assets, while the core disputes — particularly issues surrounding Iran’s nuclear program — were postponed to future negotiations.

This uncertain pattern of intermittent negotiations and escalating tensions has directly intensified stress in energy markets while indirectly influencing gold’s safe-haven appeal.

In sharp contrast to gold’s relatively modest performance, oil markets continued to rally strongly.

On Monday, crude oil prices surged approximately 3.1%, reaching multi-week highs.

The main driver remains the potential risk of disruptions in the Strait of Hormuz, one of the world’s most critical oil shipping routes.

Roughly 20% of global oil supply depends on the strait.

The head of the International Energy Agency (IEA) warned that commercial crude inventories are declining rapidly and that strategic reserves are not unlimited.

Federal Reserve policy expectations have also shifted accordingly.

Markets currently estimate the probability of at least one Fed rate hike before December at approximately 47%–51%, while new Fed Chair Kevin Warsh faces the difficult challenge of balancing inflation pressures against economic growth.

These tightening monetary policy expectations are further limiting upside potential for gold.

Against this backdrop, several financial institutions have already started adjusting their bullish gold forecasts.

JPMorgan became one of the first major banks to lower its average gold price forecast for 2026, cutting its projection sharply from US$5,708 per ounce to US$5,243 per ounce.

The revision reflects growing market concerns over weakening short-term safe-haven demand and changes in the long-term interest-rate environment.

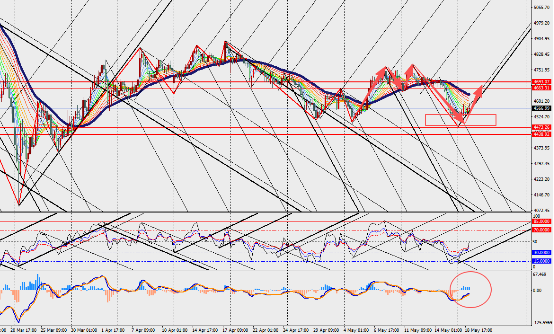

Market Analysis:

Gold rebounded after recent declines on the 4-hour chart timeframe, while both the MACD lines and histogram continue to contract below the zero axis.

Overall, the gold market is currently trapped in a delicate balance between expectations for geopolitical easing and tightening macroeconomic pressures.

Trump’s decision to pause military action has opened a window for negotiations.

If the Strait of Hormuz reopens smoothly and oil prices retreat, inflation concerns could ease, potentially exposing gold to further downside correction risks.

However, as long as Middle East tensions remain fragile and uncertain, any collapse in negotiations or signs of renewed conflict could quickly reignite safe-haven buying interest in gold.

Aiko Tanaka is our precious metals specialist with 10 years of experience in commodity markets. She holds a degree in Geology and professional certification in Commodity Market Analysis, covering gold, silver, platinum, and palladium markets with mining industry insights. Alongside her analysis, Aiko has authored thought-leadership pieces on commodities and contributes educational content aimed at new investors in the sector.

Magbasa pa