US CPI data set to show inflation cooled in June due to tumbling fuel prices

Ni FXStreet Team

Na-update: 14 Jul 2026

Sikat na Artikulo

The US Bureau of Labor Statistics (BLS) will publish the June Consumer Price Index (CPI) data on Tuesday. The report is expected to show a decline in consumer inflation, driven by the easing of crude Oil prices following the ceasefire announcement between the United States (USD) and Iran.

- The US Consumer Price Index is expected to rise by 3.8% YoY in June, down from the 4.2% advance seen in May.

- Annual core CPI inflation is expected to hold steady at 2.9%.

- EUR/USD finds support but is yet to offer a convincing sign of a bullish reversal.

The US Bureau of Labor Statistics (BLS) will publish the June Consumer Price Index (CPI) data on Tuesday. The report is expected to show a decline in consumer inflation, driven by the easing of crude Oil prices following the ceasefire announcement between the United States (USD) and Iran.

The monthly CPI is forecast to decline by 0.1%, following the 0.5% increase recorded in May, while the annual reading is seen retreating to 3.8% from 4.2% reported in the previous month, which marked the highest level since May 2023. Core CPI figures, which exclude volatile food and energy prices, are expected to post an increase of 0.2% and 2.9%, on a monthly and yearly basis, respectively, steadying compared with May.

Following a nearly 17% drop in May, Crude Oil prices declined by more than 20% in June and came back to pre-war levels, as investors cheered news of the US and Iran reaching a ceasefire on June 17 to start negotiations to bring an end to the conflict. As a result, a retreat in the monthly CPI print should not come as a surprise.

Previewing the inflation data, “June CPI likely showed inflation remained contained, with core up 0.20% m/m. Soft goods prices and further shelter normalization should keep underlying inflation steady, though this year’s Oil shock may continue to lift airfares. Risks to our forecast look more balanced than in recent reports. We expect headline CPI fell 0.22% m/m, led by a 10% drop in gasoline prices,” said TD Securities analysts.

Economic Indicator

Consumer Price Index (YoY)

Inflationary or deflationary tendencies are measured by periodically summing the prices of a basket of representative goods and services and presenting the data as The Consumer Price Index (CPI). CPI data is compiled on a monthly basis and released by the US Department of Labor Statistics. The YoY reading compares the prices of goods in the reference month to the same month a year earlier.The CPI is a key indicator to measure inflation and changes in purchasing trends. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.Next release: Tue Jul 14, 2026 12:30

Frequency: Monthly

Consensus: 3.8%

Previous: 4.2%

Source: US Bureau of Labor Statistics

The US Federal Reserve (Fed) has a dual mandate of maintaining price stability and maximum employment. According to such mandate, inflation should be at around 2% YoY and has become the weakest pillar of the central bank’s directive ever since the world suffered a pandemic, which extends to these days. Price pressures keep rising amid supply-chain issues and bottlenecks, with the Consumer Price Index (CPI) hanging at multi-decade highs. The Fed has already taken measures to tame inflation and is expected to maintain an aggressive stance in the foreseeable future.

What to expect in the next CPI data report?

Although CPI figures for June could confirm that falling Oil prices helped inflation ease, investors could overlook this development. Since the beginning of July, Oil prices have edged higher again as the US and Iran started exchanging strikes, risking the sustainability of the fragile ceasefire and reviving concerns over progress in inflation slowing down.

In addition, market participants are increasingly worried about the potential inflationary effect of the artificial intelligence (AI) boom. The massive capital wave flowing into AI infrastructure, rising industrial electricity costs and notable price premiums on tech hardware and LLM software subscriptions, could keep core services and goods inflation elevated and put pressure on consumers.

In a recently published study, the Fed pointed out that the “Computer Software and Accessories" category of the Personal Consumption Expenditures (PCE) Price Index, which is not publicly accessible, “had been falling over the past 25 years at an average annualized rate of 5.3%,” but rose at a record pace of “73% annualized increase from November 2025 through March 2026.”

Hence, even if there is a monthly decline in the CPI, as expected, investors might not see it as a convincing sign that could derail the Fed from potentially tightening the policy later in the year.

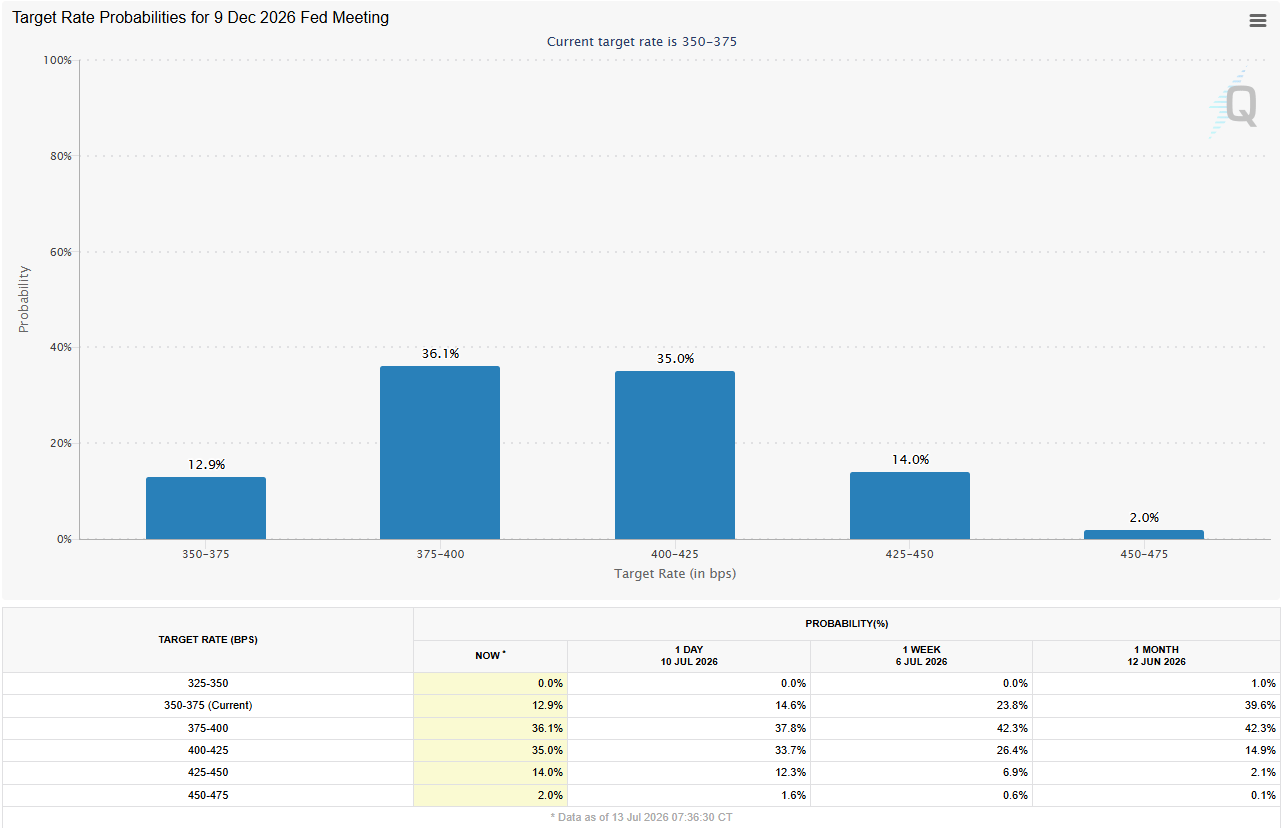

According to the CME FedWatch Tool, markets currently see about a 30% probability of a 25 basis points (bps) interest rate hike in July and price in around a 77% chance that the US central bank will raise rates at least once by the end of the year.

How could the US Consumer Price Index report affect EUR/USD?

If the monthly CPI surprises to the upside and posts a positive reading, investors could reassess the odds of a July rate hike with the immediate reaction and boost the US Dollar. In this scenario, EUR/USD could come under renewed bearish pressure.

Conversely, a bigger decline in the monthly CPI, with a reading of at least -0.2%, could hurt the USD initially and help EUR/USD gain traction. However, investors are unlikely to overreact to a single soft CPI print given that Oil prices are rising again and growing doubts surrounding the impact of AI on inflation.

Eren Sengezer, European Session Lead Analyst, shares a brief technical outlook for EUR/USD:

“EUR/USD has managed to find a foothold after touching a fresh 12-month low below 1.1330 in Late June and has stabilized slightly above 1.1400 since. However, the Relative Strength Index (RSI) indicator on the daily chart is yet to climb above 50, and the pair is yet to flip the 20-day Simple Moving Average (SMA) into support, reflecting buyers’ hesitancy.”

“On the upside, 1.1500 (round level, static level) aligns as an interim resistance level for the pair ahead of 1.1550-1.1555 (Upper arm of the Bollinger Band, 50-day SMA), 1.1600 (100-day SMA, descending trend line) and 1.1645 (200-day SMA). Looking south, the first support level could be spotted at 1.1350 (static level), followed by 1.1220 (static level, round level) and 1.1160 (static level).”

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions. The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

Higit sa isang milyong user ang umaasa sa FXStreet para sa real-time market data, charting tools, expert insights, at Forex news. Ang komprehensibong economic calendar at educational webinars nito ay tumutulong sa mga trader na manatiling may alam at gumawa ng kalkuladong mga desisyon. Sinusuportahan ang FXStreet ng humigit-kumulang 60 propesyonal sa pagitan ng Barcelona HQ at iba’t ibang rehiyon sa buong mundo.

Magbasa pa