[TMGM Financial Breakfast] Profit-Taking Pressure Weighs on Gold Prices

The U.S. Consumer Price Index (CPI) report for February came in largely in line with market expectations and had limited impact on the metals market.

In February, U.S. CPI rose 0.3% month-on-month and 2.4% year-on-year. Core CPI, which excludes food and energy, increased 0.2% month-on-month and 2.5% year-on-year. Overall inflation data remained moderate. However, potential upside risks to energy prices—driven by geopolitical conflicts—could gradually emerge in the coming months. In the short term, the direct impact on precious metals appears limited.

From a broader market perspective, the U.S. Dollar Index moved higher during the session, while crude oil futures on the New York Mercantile Exchange climbed. The benchmark 10-year U.S. Treasury yield is currently fluctuating between approximately 4.15% and 4.22%.

Oil prices surged nearly 4% to 5% after another attack on vessels in the Strait of Hormuz intensified concerns about potential supply disruptions. The International Energy Agency’s (IEA) proposal to release strategic petroleum reserves has been deemed insufficient to fully ease these concerns. Iran has reportedly continued blocking the strait and threatened to prevent any oil shipments from passing through. Actual supply disruptions could exceed 15 million barrels per day—far surpassing the short-term buffer capacity of reserve releases. Iran has also launched attacks toward Israel and other targets in the Middle East and warned that oil prices could rise to $200 per barrel.

Standard Chartered noted that it is not uncommon for gold prices to face downward pressure for several weeks amid strong cash demand. However, the bank maintains a positive long-term outlook on gold and expects prices to resume their upward trend after short-term profit-taking subsides. The gold market appears to be caught between safe-haven demand driven by geopolitical tensions and concerns over persistently high interest rates.

Goldman Sachs and JPMorgan recently reiterated that geopolitical risk premiums have significantly strengthened gold’s underlying support. If the Strait of Hormuz crisis persists for more than 30 days, gold could retest the $5,400–$5,600 range. Conversely, if tensions ease in the short term, prices may pull back toward the key psychological level of $5,000.

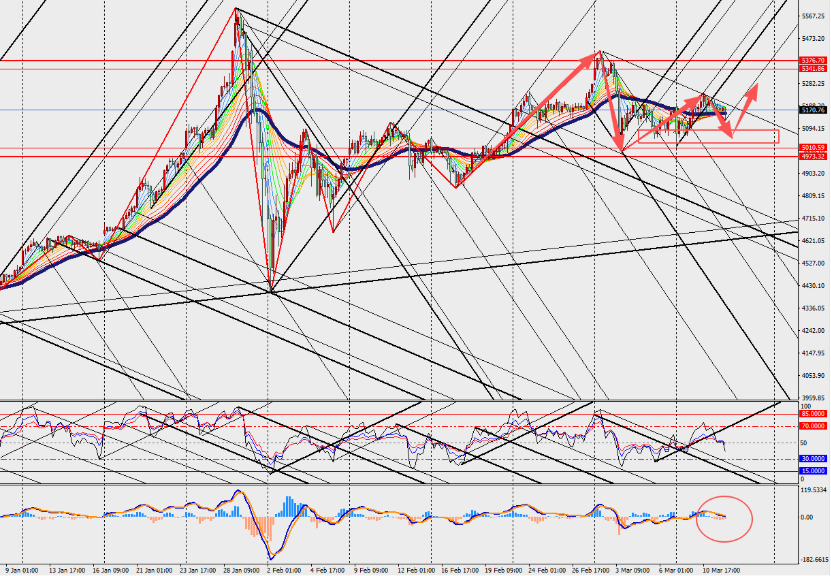

Market Analysis:

On the four-hour chart, gold has shown a rebound following a pullback, with the MACD lines and histogram converging near the zero axis. The market is closely watching the Federal Reserve’s March policy meeting and U.S. energy inventory data. Any unexpected developments in the Middle East could trigger sharp volatility. In the long term, continued central bank gold purchases and expectations of renewed inflation remain solid structural support for a bullish gold trend.