BoC set to keep interest rate unchanged, awaiting further economic data

By FXStreet Team

Updated: 29 Apr 2026

POPULAR ARTICLES

The Bank of Canada (BoC) is widely expected to keep its monetary policy rate unchanged at 2.25% for its fourth consecutive meeting on Wednesday, requesting more time to assess the impact on inflation and economic growth from the US-Iran war.

- The Bank of Canada is widely expected to leave the interest rate unchanged at 2.25%.

- Policymakers will require more time to assess the impact of the Middle East war.

- Investors will be attentive to the bank’s inflation expectations for Canada.

The Bank of Canada (BoC) is widely expected to keep its monetary policy rate unchanged at 2.25% for its fourth consecutive meeting on Wednesday, requesting more time to assess the impact on inflation and economic growth from the US-Iran war. A shift in long-term inflation expectations emerging from higher energy prices due to the Middle East conflict could trigger the next big reaction in the Canadian Dollar (CAD).

The BoC left its monetary policy unchanged at its previous meeting in March and removed forward guidance references that the current rate is appropriate. The bank’s statement noted that economic growth had weakened in the first quarter of the year and that the energy shock from the Middle East war would keep prices at high levels in the near-term

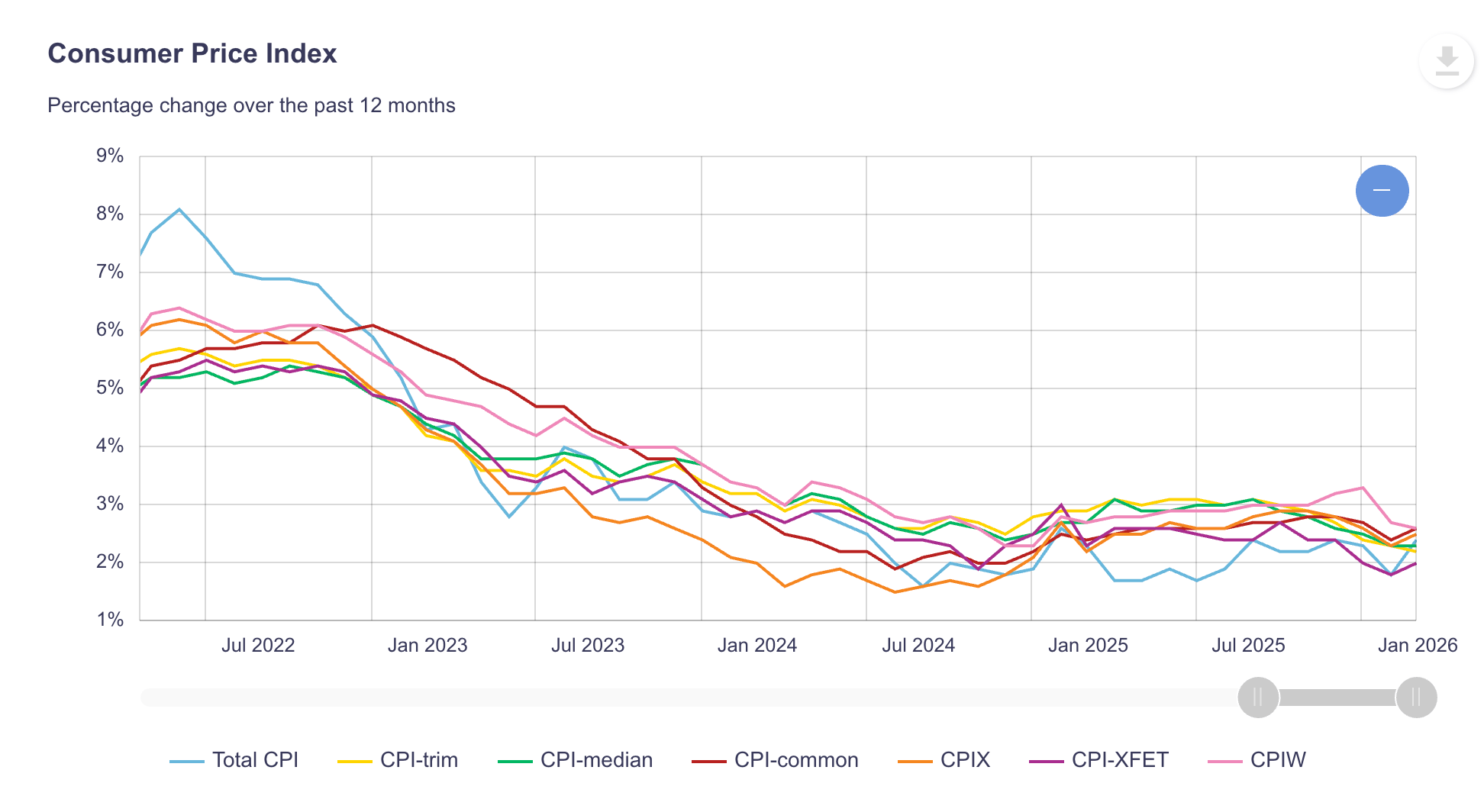

Canada’s Consumer Prices Index (CPI) figures from March confirmed those views. Inflation accelerated to a 2.4% year-on-year rate from 1.8% in February, exceeding the BoC’s 2% target, yet falling short of the 2.5% expected by the market, which provides the central banks with some leeway to wait for additional data.

The BoC Governor, Tiff Macklem, practically discarded any immediate monetary policy reaction earlier in April. Macklem said that he is not concerned about the short-term spike in prices. The central bank’s latest CPI projections foresee inflationary pressures easing to 2.2% by the end of the year and 2.1% in 2027.

Furthermore, Canadian economic growth is starting to stutter with the trade relationship with its main partner, the United States (US), under review. The Gross Domestic Product (GDP) contracted at a 0.6% annualized pace in the fourth quarter of 2025. The monthly GDP barely rose 0.1% in January, according to the latest data released, and the IVEY Purchasing Manager’s Index (PMI) seasonally adjusted unexpectedly fell into contraction levels in March, suggesting that growth has remained sluggish in the first months of 2026. Unless this scenario changes radically, monetary tightening is likely to be off topic.

Looking forward, market analysts at TD Securities expect the BoC interest rate to remain steady for the foreseeable future: "We still expect the BoC to stay on hold for the rest of 2026, especially given the downside surprise on recent CPI. The recent moves higher in rates, particularly in BoC pricing further out, should be seen more as a function of importing the pricing out of Fed rate cuts rather than an accurate reflection of a change of outlook. December is currently priced in at 2.61%, and a return to pre-war levels will likely be slower rather than traded off a single dovish data point or communication."

When will the BoC release its monetary policy decision, and how could it affect USD/CAD?

The Bank of Canada will announce its policy decision on Wednesday at 13:45 GMT, and a press conference by Governor Tiff Macklem will ensue from 14:30 GMT onwards.

A report released by Reuters earlier this week revealed that the market is practically fully pricing steady interest rates after the April meeting, with 76% of the polled analysts expecting no change in the monetary policy in 2026.

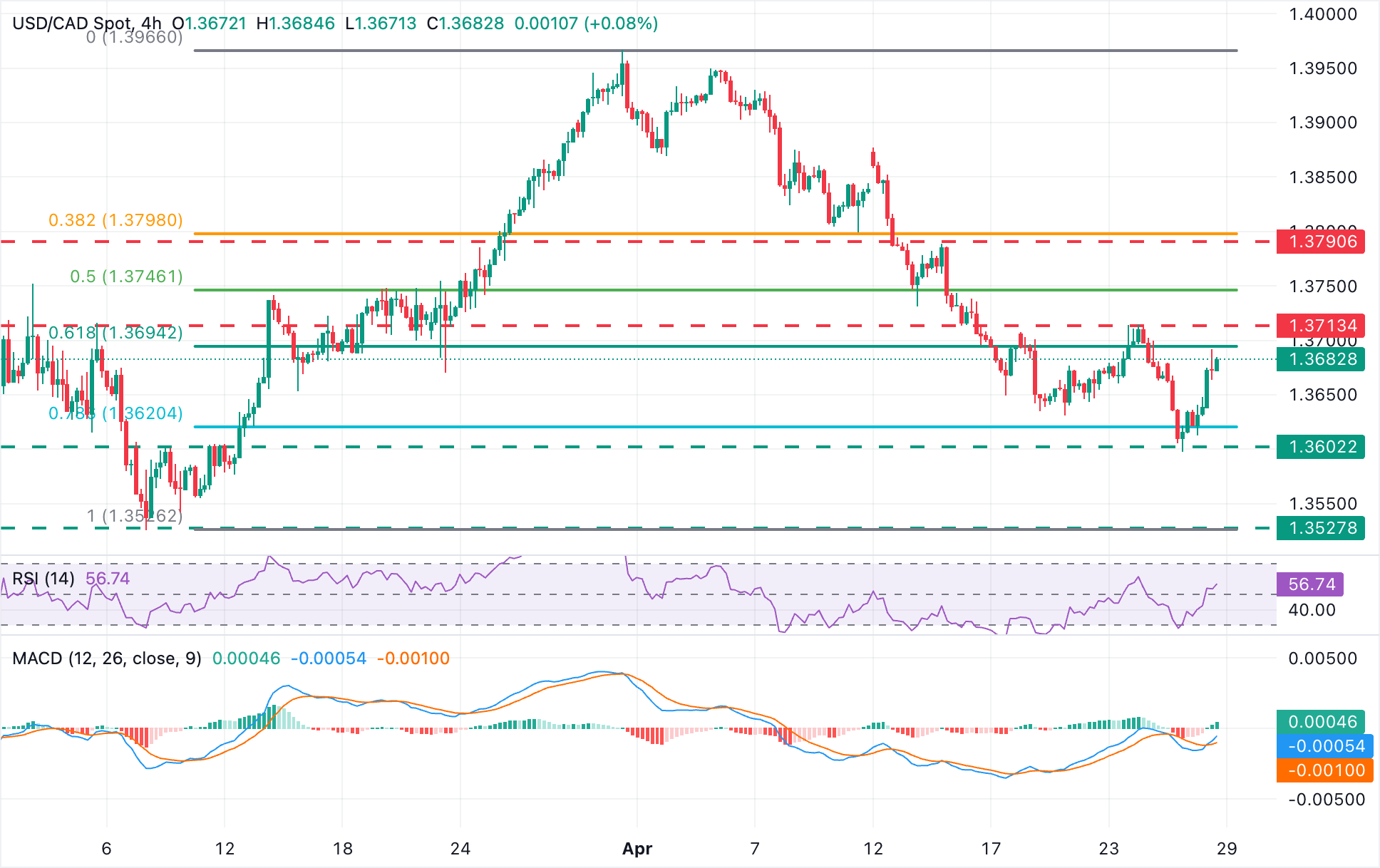

The USD/CAD has been trading within a bearish channel since peaking near 1.4000 in late March. The pair has bounced up from nearly seven-week lows, at 1.3605, but upside attempts remain seen as good entry opportunities for sellers, rather than real recovery attempts.

On the upside, Guillermo Alcalá, FX Analyst at FXStreet.com, expects bulls to be challenged at the resistance area above 1.3700. “The pair found some support near 1.3600 to trim losses as the US Dollar (USD) picks up ahead of the Federal Reserve’s (Fed) meeting, which is also due on Wednesday. The pair, however, is likely to meet resistance at last week’s highs, right above the 1.3700 level. A confirmation above that level would signal a deeper recovery towards a previous support-turned-resistance in the area of 1.3800.

A rejection at those levels would confirm the bearish trend, according to Alcala: “The pair has reached the 78.6% Fibonacci retracement of the March bull run, a common target for corrections, but has not given clear signs of a trend shift as of yet. In this sense, Monday´s low, at 1.3597, remains on the bears' radar. Further down, the pair would need a dovish Fed or an even more unlikely hawkish surprise by the BoC, to extend losses towards the confluence of the channel bottom with March 9 lows, at the 1.3525 area.”

Central banks FAQs

Central Banks have a key mandate which is making sure that there is price stability in a country or region. Economies are constantly facing inflation or deflation when prices for certain goods and services are fluctuating. Constant rising prices for the same goods means inflation, constant lowered prices for the same goods means deflation. It is the task of the central bank to keep the demand in line by tweaking its policy rate. For the biggest central banks like the US Federal Reserve (Fed), the European Central Bank (ECB) or the Bank of England (BoE), the mandate is to keep inflation close to 2%.

A central bank has one important tool at its disposal to get inflation higher or lower, and that is by tweaking its benchmark policy rate, commonly known as interest rate. On pre-communicated moments, the central bank will issue a statement with its policy rate and provide additional reasoning on why it is either remaining or changing (cutting or hiking) it. Local banks will adjust their savings and lending rates accordingly, which in turn will make it either harder or easier for people to earn on their savings or for companies to take out loans and make investments in their businesses. When the central bank hikes interest rates substantially, this is called monetary tightening. When it is cutting its benchmark rate, it is called monetary easing.

A central bank is often politically independent. Members of the central bank policy board are passing through a series of panels and hearings before being appointed to a policy board seat. Each member in that board often has a certain conviction on how the central bank should control inflation and the subsequent monetary policy. Members that want a very loose monetary policy, with low rates and cheap lending, to boost the economy substantially while being content to see inflation slightly above 2%, are called ‘doves’. Members that rather want to see higher rates to reward savings and want to keep a lit on inflation at all time are called ‘hawks’ and will not rest until inflation is at or just below 2%.

Normally, there is a chairman or president who leads each meeting, needs to create a consensus between the hawks or doves and has his or her final say when it would come down to a vote split to avoid a 50-50 tie on whether the current policy should be adjusted. The chairman will deliver speeches which often can be followed live, where the current monetary stance and outlook is being communicated. A central bank will try to push forward its monetary policy without triggering violent swings in rates, equities, or its currency. All members of the central bank will channel their stance toward the markets in advance of a policy meeting event. A few days before a policy meeting takes place until the new policy has been communicated, members are forbidden to talk publicly. This is called the blackout period.

Economic Indicator

BoC Interest Rate Decision

The Bank of Canada (BoC) announces its interest rate decision at the end of its eight scheduled meetings per year. If the BoC believes inflation will be above target (hawkish), it will raise interest rates in order to bring it down. This is bullish for the CAD since higher interest rates attract greater inflows of foreign capital. Likewise, if the BoC sees inflation falling below target (dovish) it will lower interest rates in order to give the Canadian economy a boost in the hope inflation will rise back up. This is bearish for CAD since it detracts from foreign capital flowing into the country.

Read more.Next release: Wed Apr 29, 2026 13:45

Frequency: Irregular

Consensus: 2.25%

Previous: 2.25%

Source: Bank of Canada

More than a million users rely on FXStreet for real-time market data, charting tools, expert insights, and forex news. Its comprehensive economic calendar and educational webinars help traders stay informed and make calculated decisions. FXStreet is supported by a team of about 60 professionals, split between the Barcelona headquarters and various global regions.

Read More