TMGM: ECB Holds Rates as Internal Divisions Widen; EUR/USD Slips on Choppy Trade

In a statement, the ECB said that despite a challenging global backdrop, the economy continues to grow. It added that the labor market remains strong and private-sector balance sheets are solid. With inflation still close to the 2% medium-term target, the Bank described the inflation outlook as broadly unchanged.

Even so, persistent global trade disputes and geopolitical tensions keep the outlook uncertain. The ECB’s steady hand signals confidence that inflation and growth are on a sustainable path. As a result, Europe’s policy stance is unlikely to deliver major surprises and should remain aligned with market pricing—meaning the trajectories of the euro, European equities, and bonds will largely hinge on developments in U.S. policy and markets.

Nevertheless, some policymakers believe downside risks to growth and inflation are larger, providing grounds for further easing. Financial investors share the concern, assigning a 40%–50% probability to another rate cut before next summer.

By contrast, policy hawks argue that Germany’s ramp-up in defense and infrastructure spending fundamentally changes the outlook and could lift growth and prices even without additional ECB action. President Lagarde noted that long-term inflation expectations hover around 2%, but the outlook is more uncertain than usual; increased defense spending may push inflation higher in the medium term.

According to Eurostat on Thursday, following France’s fastest output growth since 2023, eurozone Q3 GDP rose 0.2%, beating market expectations.

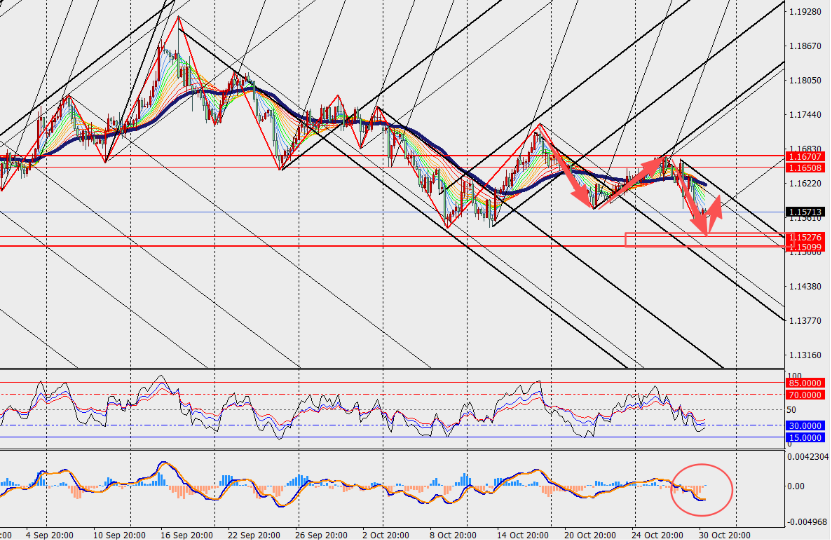

Market View (EUR/USD):

On the H4 timeframe, EUR/USD is retreating in choppy trade, with MACD lines and histogram narrowing below the zero line. After euro-area annual inflation climbed to 2.2% in September, it is expected to ease slightly to 2.1% this month. The ECB will publish new economic projections in December, extending the forecast horizon to 2028, which should provide a deeper discussion of these issues.