What is keeping the Japanese Yen at 40-year lows as Tankan surges and authorities watch from the sidelines?

Di FXStreet Insights Team

Aggiornato: 1 Jul 2026

ARTICOLI POPOLARI

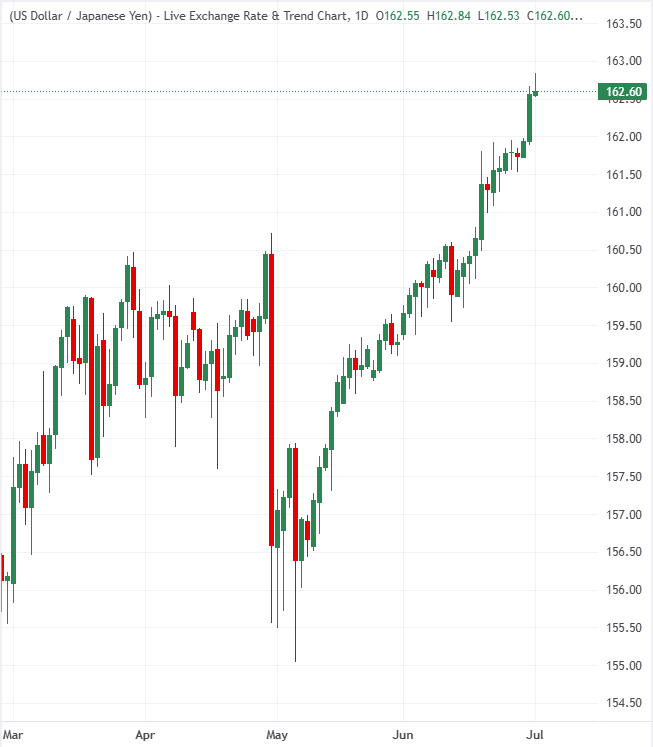

The Japanese Yen (JPY) continues to trade near levels last seen in 1986 against the US Dollar.

The Japanese Yen (JPY) continues to trade near levels last seen in 1986 against the US Dollar. Despite strong domestic economic indicators – headlined by a robust quarterly Tankan survey – the Yen remains heavily weighed down by aggressive short positioning and its role as a primary funding currency for global carry trades.

As the market heads into a low-liquidity US holiday weekend, speculation is high regarding whether Japan's Ministry of Finance (MoF) will strike with fresh foreign exchange interventions, or if the currency will continue its slow, controlled grind lower until the Bank of Japan (BoJ) aggressively accelerates its interest rate hiking cycle.

The ghost of summer 2024 and the new 165 line in the sand

Macro strategists at Societe Generale emphasize that the current market environment features a dangerous accumulation of speculative Yen shorts, drawing striking parallels to the volatile unwind that caught investors off guard exactly two years ago in July 2024. While the technical upside for USD/JPY remains fundamentally intact, analysts suggest that the threshold for official pushback has shifted higher, though unexpected shifts in US Federal Reserve policy could easily spark an abrupt short-covering squeeze.

July carries ugly memories for Yen shorts and those investors with memories of how events turned against them in the summer of 2024 will be inclined to tread carefully against another backdrop of aggressive bearish positioning.

Why direct FX interventions are only a temporary band-aid

Rabobank argues that unilateral market interventions by the Japanese MoF will ultimately fail to reverse the Yen's deeply ingrained negative sentiment on their own. For the currency to establish a sustainable floor and dismantle the highly lucrative carry trades currently driving capital out of Japan, monetary policymakers must actively step up with more hawkish rate guidance.

In our view, the BoJ may have to signal it is prepared to accelerate the pace of rate hikes before the JPY finds decent support in order to break the market’s attachment to the JPY as a funding currency for carry trades.

Resilient Tankan data contrasts with a tolerated, slow market grind

MUFG points out that the BoJ’s latest outperforming Tankan report firmly justifies a more aggressive policy tightening schedule than what the broader market is currently pricing in. The recent softening of verbal intervention warnings from Japanese officials suggests that authorities may comfortably tolerate a steady, low-volatility climb in USD/JPY, provided the broader bond and equity markets remain stable.

The quarterly Tankan report, released from the BoJ today was stronger than expected and certainly endorses the rate hike by the BoJ in June and strengthens the case for further hikes going forward.

Banks anticipate immediate holiday volatility risks ahead of gradual recovery

The banks emphasize an imminent risk of intervention over the thinned Friday holiday conditions. While Societe Generale and MUFG note that the MoF might stay on the sidelines if the pace of Yen selling remains orderly, they warn that any sudden spike in illiquid holiday trading could prompt a sudden defensive strike.

Looking further out on a three-month horizon, Rabobank projects a moderate recovery for the currency – targeting a move back down to 159 for the USD/JPY pair – under the structural assumption that a structurally hawkish BoJ will eventually step in to backstop the sliding currency.

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor.)

Oltre un milione di utenti si affida a FXStreet per dati di mercato in tempo reale, strumenti di charting, approfondimenti di esperti e notizie Forex. Il loro calendario economico completo e i webinar formativi aiutano i trader a rimanere informati e a prendere decisioni ponderate. FXStreet conta circa 60 professionisti tra la sede di Barcellona e diverse regioni globali.

Leggi di più