Gold Stuck Below $4,600 in the Short Term, but Long-Term Bullish Bets Remain Intact

Uncertainty in the global macro environment is continuing to rise, while central banks around the world are finding their policy flexibility increasingly constrained between controlling inflation and supporting growth. This environment raises the probability of policy mistakes — and historically, such risks have often been major catalysts for gold rallies.

Gold’s recent failure to rally significantly amid geopolitical tensions does not necessarily mean its safe-haven status has weakened. Instead, the weakness appears to reflect tighter market liquidity conditions and forced selling triggered by margin pressure, rather than deterioration in underlying fundamentals.

Central banks are facing increasingly difficult trade-offs in controlling inflation. Aggressive rate hikes risk further weakening economic growth and potentially triggering stagflation, leaving policymakers with limited flexibility on the interest-rate path.

Relying solely on interest-rate policy is becoming less effective in addressing today’s complex economic environment. Policymakers are well aware that interest-rate tools alone are unlikely to solve current challenges without causing broader economic pain.

At the same time, the growing number of policy objectives and shorter policy cycles may increase the likelihood of policy errors. Attempting to achieve multiple goals simultaneously within a compressed timeframe amplifies uncertainty — and that uncertainty itself tends to support gold prices.

Beyond monetary policy, recession risk remains another key variable. Any visible signs of economic slowdown would likely provide strong support for gold.

Rising global government debt levels and long-term depreciation pressure on the U.S. dollar also continue to support precious metals structurally. As fiscal pressure intensifies, structural currency debasement could re-emerge as a long-term theme.

On the demand side, Asia remains a core pillar of support. While high prices have weighed somewhat on jewelry demand, physical demand from China and India has not disappeared. Instead, demand is increasingly shifting toward more investment-oriented forms of gold consumption.

Institutional investors are also reassessing gold’s role within portfolios. After years of underallocation, more investors are recognizing that lacking exposure to gold weakens diversification benefits. Gold’s role is gradually evolving from a traditional safe-haven asset into a partial alternative to fixed income, especially amid rising volatility in bond markets.

Central bank buying further reinforces this trend. Gold’s combination of liquidity and political neutrality is making it increasingly attractive as a reserve asset, strengthening its long-term appeal.

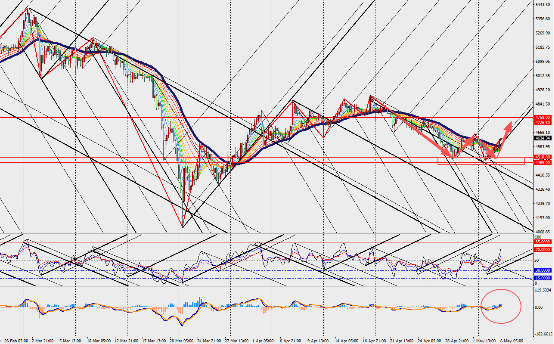

Market Interpretation

On the four-hour chart, gold is showing a short-term rebound, with MACD lines and volume bars expanding near the zero axis.

Gold remains highly sensitive to market expectations surrounding Federal Reserve policy. If market consensus and forward guidance shift toward a more dovish stance, gold could regain support even if interest rates remain unchanged in the short term.

At present, money markets may be waiting for a meaningful peace agreement between the U.S. and Iran before repricing expectations for future rate cuts.