US CPI data set to show inflation at three-year high in May, backing Fed hawkish tilt

โดย FXStreet Team

อัปเดตแล้ว: 10 Jun 2026

บทความยอดนิยม

The US Bureau of Labor Statistics (BLS) will publish the May Consumer Price Index (CPI) data on Wednesday. The report is expected to show another step up in consumer inflation, driven by the persistently high Oil prices due to the ongoing crisis in the Middle East.

- The US Consumer Price Index is expected to rise 4.2% YoY in May as energy prices remain persistently high.

- Annual core CPI inflation is expected to edge higher to 2.9%.

- EUR/USD bounced from a two-month low, but the bullish case is still limited.

The US Bureau of Labor Statistics (BLS) will publish the May Consumer Price Index (CPI) data on Wednesday. The report is expected to show another step up in consumer inflation, driven by the persistently high Oil prices due to the ongoing crisis in the Middle East.

The monthly CPI is forecast to rise 0.5%, following the 0.6% increase recorded in April, while the annual reading is seen climbing to its highest level since May 2023 at 4.2%, from 3.8% in April. Core CPI figures, which exclude volatile food and energy prices, are expected to post an increase of 0.3% and 2.9%, on a monthly and yearly basis, respectively.

Crude Oil prices are up more than 50% since the beginning of the conflict in the Middle East on February 28. Although there was a sharp downward correction in Oil prices in late April after the United States (US) and Iran came to terms to stop military activity and start negotiations to permanently end the war, the lack of progress in talks and a renewed escalation of tensions allowed the West Texas Intermediate (WTI) prices to remain high.

In response to Israel’s heightened aggression in Lebanon, Iran fired missiles at Israel on Sunday, June 7. The Israeli military launched a retaliatory attack, hitting military targets in western and central Iran. This development marked the first exchange of strikes since the temporary ceasefire agreement was reached.

Previewing the inflation data, “we look for core CPI inflation to take a breather in May following the shelter-led jump that saw the series surge to 0.38% m/m in April. Services price normalization should more than offset a small pickup in goods inflation, despite our expectation for airfares to gain additional strength. Energy prices remained firm owing to the passthrough from still high oil prices,” said TD Securities analysts.

What to expect in the next CPI data report?

CPI figures for May will provide key clues regarding the impact of persistently high Oil prices on consumer inflation. Since this is largely anticipated, core inflation figures will help markets understand at what rate rising energy costs are spilling over into the broader economy and driving up the prices of other goods and services.

A reading above the market expectation of 0.3% in the monthly core CPI could feed into concerns over high inflation getting entrenched in the economy. Conversely, a print below analysts’ forecast could ease fears over prices getting out of control.

Still, even in this latter scenario, investors are unlikely to be convinced of a steady decline in inflation unless the US-Iran crisis ends and Oil prices return to pre-war levels. Even if the Strait of Hormuz reopens soon, it remains highly uncertain how long it will take for Oil supplies to hit full capacity and thus prices to fall to pre-war levels.

In the meantime, Federal Reserve (Fed) policymakers have room to stay focused on taming inflation after consecutive months of impressive labor market data. Hence, a soft print by itself is unlikely to alter market expectations of a hawkish policy shift in a significant way.

The latest data published by the BLS showed that Nonfarm Payrolls (NFP) rose by 172K in May. This print followed the 179K increase (revised from 115K) recorded in April and surpassed the market expectation of 85K by a wide margin.

How could the US Consumer Price Index report affect EUR/USD?

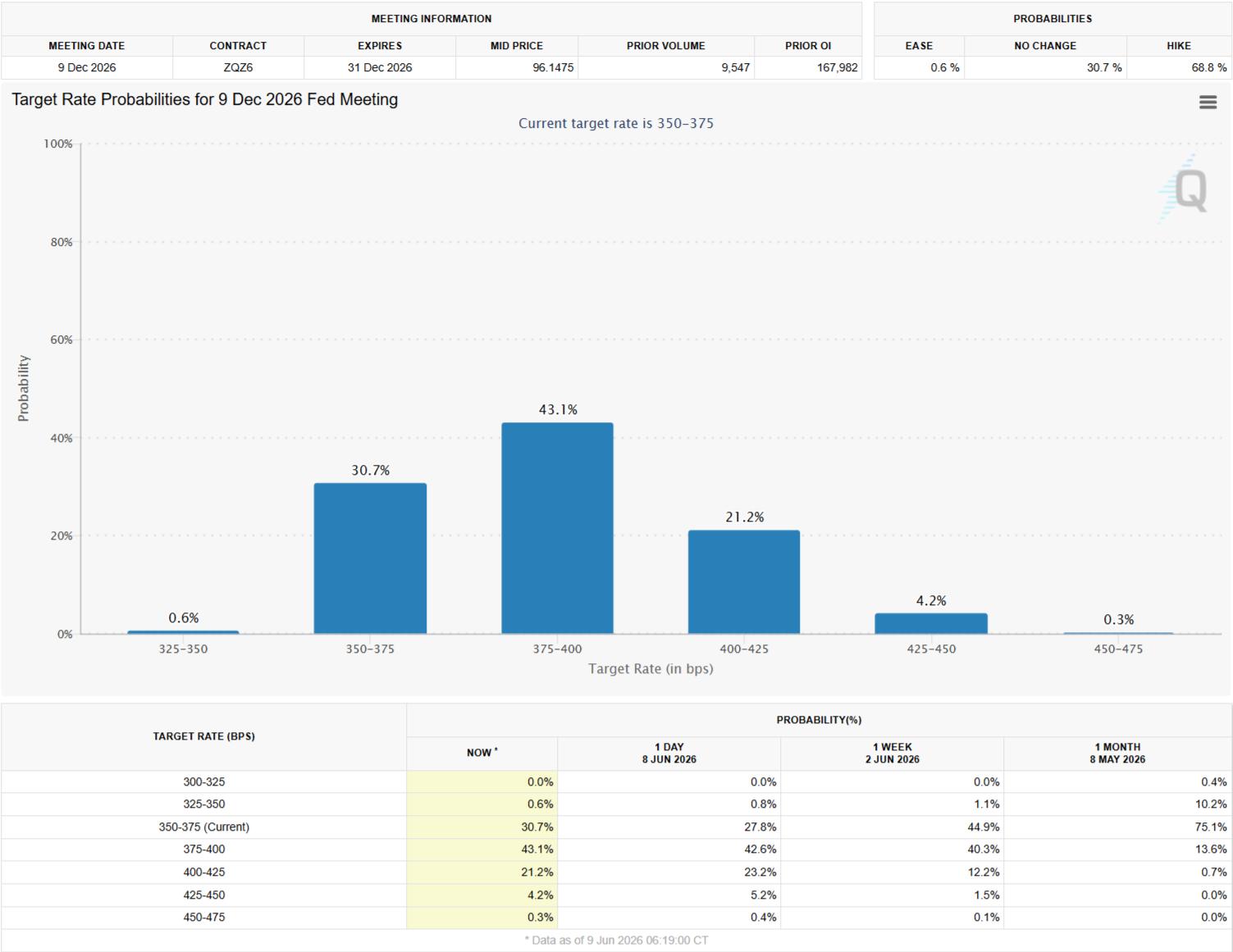

Markets currently see about a 70% chance that the Fed will hike the policy rate by 25 basis points (bps) at least once by the end of the year, according to the CME FedWatch Tool. Moreover, there is about a 38% chance that the rate hike might come as early as September.

A stronger-than-forecast monthly core CPI print for May could lift the odds of an interest rate increase in September. In this scenario, the US Dollar (USD) could gather strength with the immediate reaction.

On the other hand, a soft core CPI print could have the opposite effect on the USD’s valuation. Still, any negative impact on the USD could remain short-lived and cap any potential recovery gains in EUR/USD.

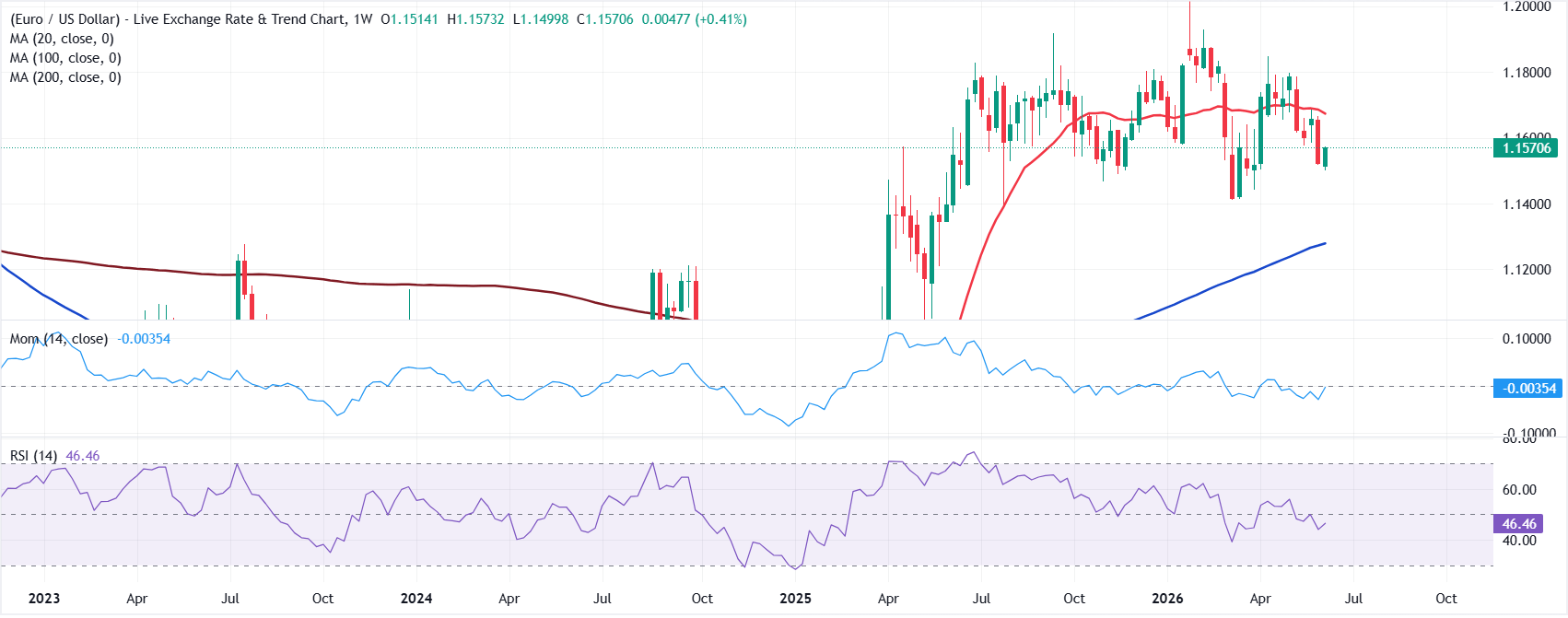

Valeria Bednarik, FXStreet Chief Analyst, notes: “The EUR/USD pair found buyers around the 1.1500 mark and bounced, but the recovery fell short of erasing the bearish tone of the pair. Selling pressure receded, but a steeper recovery remains out of the picture, according to technical readings in the weekly chart, which shows that the pair develops well below a mildly bearish 20-week Simple Moving Average (SMA) at around 1.1670. The same chart shows technical indicators ticked higher, but remain below their midlines while lacking directional strength.”

Bednarik adds: “The immediate upward barrier is the 1.1600 threshold, ahead of the aforementioned dynamic resistance at 1.1670. Additional gains seem unlikely in the current scenario, yet the next area to watch should the advance continue is the 1.1740 price zone. The 1.1500 mark is an immediate support level, with a more relevant one at 1.1470, a long-term static support area. A clear break below the latter should open the door to a steeper decline towards the 1.1400 region.”

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions. The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

Economic Indicator

Consumer Price Index (MoM)

Inflationary or deflationary tendencies are measured by periodically summing the prices of a basket of representative goods and services and presenting the data as The Consumer Price Index (CPI). CPI data is compiled on a monthly basis and released by the US Department of Labor Statistics. The MoM figure compares the prices of goods in the reference month to the previous month.The CPI is a key indicator to measure inflation and changes in purchasing trends. Generally, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.Next release: Wed Jun 10, 2026 12:30

Frequency: Monthly

Consensus: 0.5%

Previous: 0.6%

Source: US Bureau of Labor Statistics

The US Federal Reserve (Fed) has a dual mandate of maintaining price stability and maximum employment. According to such mandate, inflation should be at around 2% YoY and has become the weakest pillar of the central bank’s directive ever since the world suffered a pandemic, which extends to these days. Price pressures keep rising amid supply-chain issues and bottlenecks, with the Consumer Price Index (CPI) hanging at multi-decade highs. The Fed has already taken measures to tame inflation and is expected to maintain an aggressive stance in the foreseeable future.

ผู้ใช้กว่าหนึ่งล้านคนพึ่งพา FXStreet สำหรับข้อมูลตลาดเรียลไทม์ เครื่องมือกราฟ การวิเคราะห์จากผู้เชี่ยวชาญ และข่าวฟอเร็กซ์ ปฏิทินเศรษฐกิจที่ครอบคลุมและเว็บบินาร์การศึกษาช่วยให้เทรดเดอร์ทันเหตุการณ์และตัดสินใจอย่างรอบคอบ FXStreet มีทีมงานประมาณ 60 คน แบ่งระหว่างสำนักงานใหญ่บาร์เซโลนาและภูมิภาคต่าง ๆ ทั่วโลก

อ่านเพิ่มเติม