British Pound Sterling banks a peace rally as the bills come due

By Joshua Gibson

Updated: 11 Jun 2026

POPULAR ARTICLES

The British Pound spent most of Thursday doing what everything else did, leaking lower while Washington and Tehran traded fire, then exploding higher when President Trump canceled the evening's planned strikes just after 17:30 GMT and declared a deal all but done.

- GBP/USD jumped more than a big figure after Trump canceled a third night of strikes on Iran.

- Friday brings UK GDP with a contraction expected, the first test of a rally the Pound did nothing to earn.

- Next week compresses UK CPI, the Fed and the BoE into 48 hours, with both central banks parked on the same rate.

The British Pound spent most of Thursday doing what everything else did, leaking lower while Washington and Tehran traded fire, then exploding higher when President Trump canceled the evening's planned strikes just after 17:30 GMT and declared a deal all but done. GBP/USD gained more than a full big figure off the lows, and not one pip of it was earned in the UK.

That matters more for Cable than most, because the Pound now has to defend a borrowed rally through one of the heaviest scheduled stretches on the calendar. What the geopolitical whipsaw handed over on Thursday, the data gets to question from Friday morning onward.

Canceled by post, confirmed by no one

The shape of the day was the same across markets. US strikes ran Tuesday and Wednesday, Tehran answered at American bases across the Gulf, and Trump opened Thursday threatening to seize Kharg Island before canceling the night's raids and claiming approval on a meaningful deal at the highest level of Iranian leadership.

Iran has confirmed nothing. Its semiofficial Fars agency first reported that no text had been approved, then floated high odds of approval since Washington accepted Iran's own draft, while Trump talks up a weekend signing in Europe with the Strait of Hormuz reopening on signature. One capital is planning a ceremony; the other is publishing odds.

Washed-out momentum, intact gains

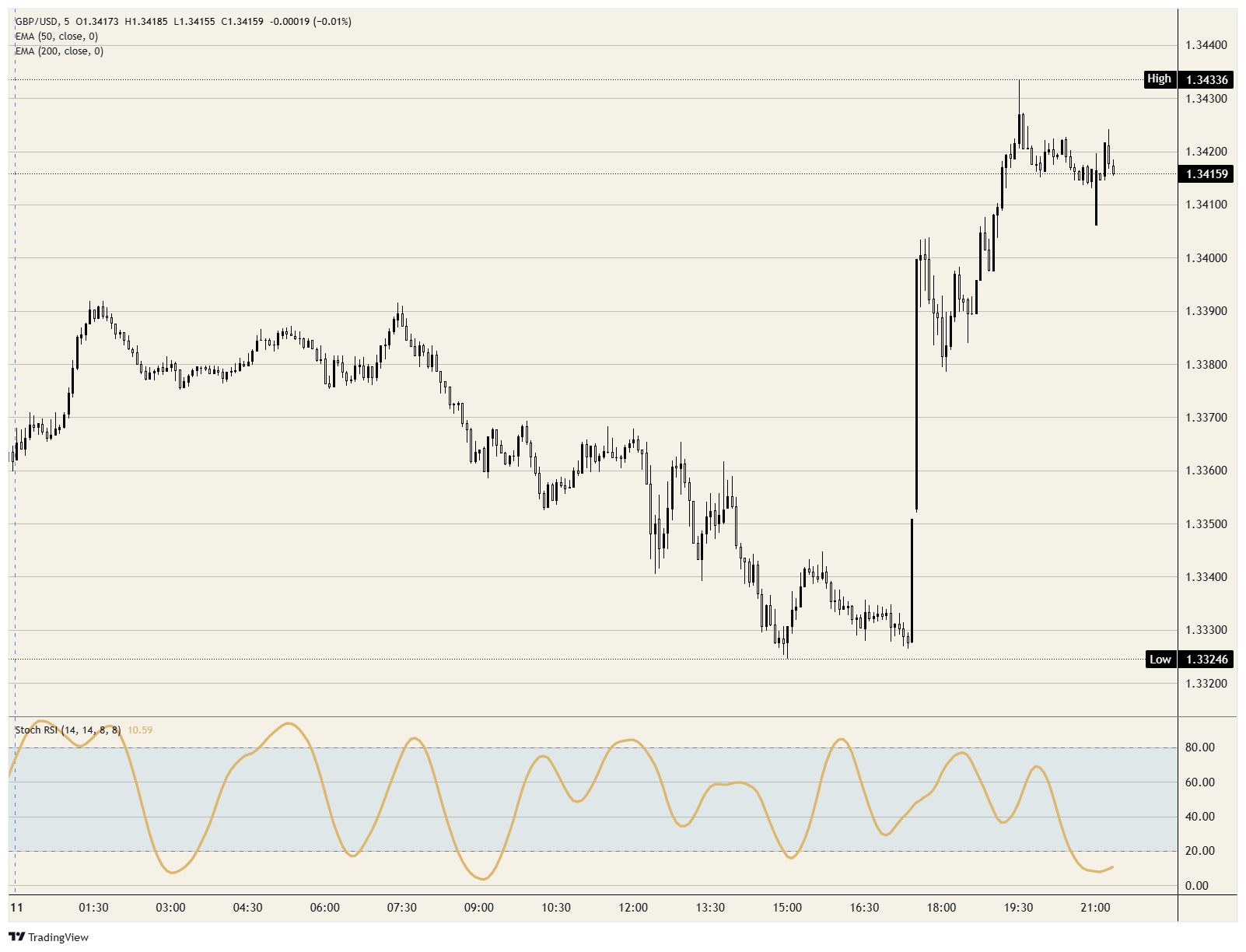

The chart work was done in one impulse. Cable leaked from just below 1.3400 in the London morning into the low 1.3300s by mid-afternoon, then the cancellation candle carved straight back through the range, cleared 1.3400 and stalled short of 1.3450.

The daily chart explains both of those numbers. Thursday's candle closed back above the 200-day Exponential Moving Average (EMA), which sits on the 1.3400 handle, while the rally stalled directly beneath the falling 50-day EMA near 1.3450. That leaves Cable wedged between its two most-watched averages, about as literal as technical tension gets.

Momentum supplies a further wrinkle, because the intraday Stochastic Relative Strength Index (Stoch RSI) has collapsed into oversold territory while price has barely surrendered anything above 1.3400. That reset usually favors the side holding the gains; the headlines decide which way it fires.

Friday's growth check comes first

The first bill lands at 06:00 GMT with monthly Gross Domestic Product (GDP) for April, where consensus expects a -0.1% MoM contraction after 0.3% growth. Industrial Production is seen barely positive, Manufacturing Production is expected to give back part of a strong prior month, and Consumer Inflation Expectations follow from a 3.2% base.

The afternoon belongs to the US side, where the University of Michigan's preliminary June sentiment is expected to improve and the accompanying inflation-expectations readings, last near 4.8% on the one-year horizon, double as a referendum on how much war is baked into American price psychology. With Crude Oil unwinding its premium, those expectation lines are suddenly the most interesting numbers on the page.

Next week, two banks and one number

Wednesday stacks UK Consumer Price Index (CPI) for May, last at 2.8% YoY, against the Federal Reserve (Fed) decision at 18:00 GMT the same evening. No change is expected to the 3.75% policy rate, but the projections are the event: the last set penciled rates ending the year below where they stand today, a promise that hot, war-flavored inflation prints, including Thursday's 6.5% YoY Producer Price Index (PPI), have been eating ever since.

Seventeen hours later, the Bank of England (BoE) answers from the identical 3.75% setting, with fresh UK jobs numbers landing at breakfast and one policymaker already voting for a hike at the last meeting. Two central banks on the same rate, deciding within a day of each other, against an inflation shock that may or may not have just ended by social media post: that is the setup Cable carries its borrowed gains into. UK Retail Sales close the week from a -1.3% prior.

Levels for a loaded calendar

Upside: Holding 1.3400 keeps 1.3450 in play, and a Tehran-confirmed weekend signing paired with a UK growth beat opens the road toward 1.3500.

Downside: A slip back through 1.3400 would unwind the 200-day EMA reclaim within a day; an Iranian denial or an ugly GDP print targets 1.3350 first, with the 1.3300 handle the fuller round trip.

Bias: Constructive above 1.3400 while the peace tape holds, but this is the major with the most scheduled ways to lose its gains, so let the calendar set the position size.

GBP/USD 5-minute chart

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

More than a million users rely on FXStreet for real-time market data, charting tools, expert insights, and forex news. Its comprehensive economic calendar and educational webinars help traders stay informed and make calculated decisions. FXStreet is supported by a team of about 60 professionals, split between the Barcelona headquarters and various global regions.

Read More