"The Yen's failure to strengthen will keep pressure to intervene": MUFG says BoJ hike alone won't break 160

By FXStreet Insights Team

Updated: 16 Jun 2026

POPULAR ARTICLES

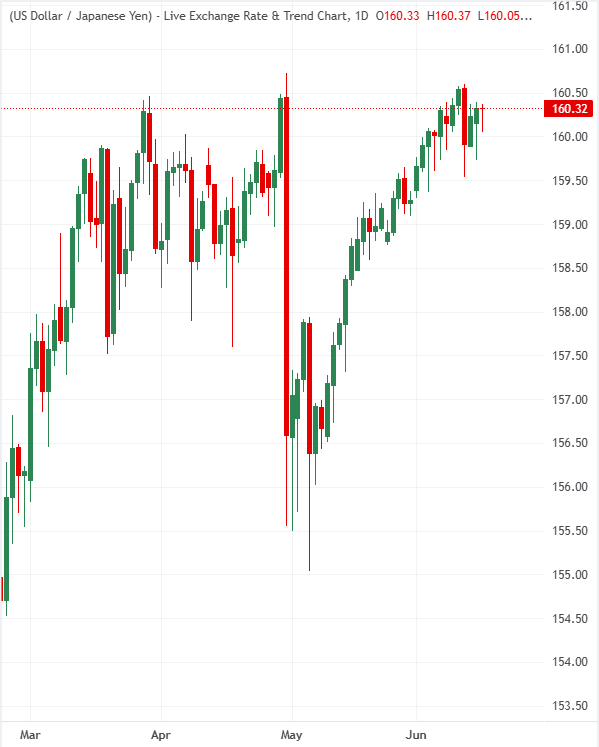

The Japanese Yen (JPY) remains anchored around the critical 160.00 threshold against the US Dollar despite the Bank of Japan's (BoJ) historic decision to raise its benchmark interest rate to 1.00%.

The Japanese Yen (JPY) remains anchored around the critical 160.00 threshold against the US Dollar despite the Bank of Japan's (BoJ) historic decision to raise its benchmark interest rate to 1.00%.

While the 25-basis-point increase lifts borrowing costs to their highest level in over three decades, its immediate market impact has been highly muted because the adjustment was already fully priced in by market participants.

However, with the central bank highlighting growing concerns over upside inflation risks and mapping out a revised path for its long-term bond-purchasing program, prominent financial institutions indicate that a structural cycle of monetary normalization will ultimately reshape the currency's trajectory.

Telegraphed tightening leaves the Yen range-bound

Macro strategy experts at MUFG observe that the Yen failed to spark a meaningful recovery immediately following the policy announcement due to the central bank's heavy pre-meeting signaling. They point out that while rapid price pass-through from global energy costs is fueling domestic inflation pressures, the BoJ's decision to pause its quantitative easing taper starting in FY2027 shows a measured approach that could leave the currency exposed to speculative selling before additional rate hikes materialize.

The weak yen is one factor which could encourage the BoJ to speed up the pace of rate hikes but there was no strong indication over the timing of the next hike at today’s policy meeting. The yen’s failure to strengthen on the back of today’s BoJ rate hike will keep pressure on Japan to intervene again to provide support.

Successive hikes lay groundwork for medium-term recovery

The research team at Societe Generale argues that a policy rate of 1.00% represents merely the bottom of Japan's neutral interest rate range. They project that persistent upward deviations in inflation will validate a steady, predictable tightening cycle over the next several quarters, which will steadily chip away at the wide yield gaps currently penalizing the Yen.

Our house view is for the policy rate to increase at a cadence of 25bp every quarter to reach the terminal policy point of 2% by the end of next year.

Banks point toward near-term vulnerability ahead of turnaround

Both institutions anticipate a soft near-term trend for the Japanese Yen, while remaining constructive on its structural path over the medium term. MUFG flags immediate downside risks, noting that a lack of aggressive dollar selling will likely keep the USD/JPY pair hovering precariously above 160.00 and necessitate fresh government market interventions.

In contrast, Societe Generale maintains that the currency is poised for an eventual turnaround, concluding that as successive quarterly hikes push the terminal policy rate toward 2.00% by the end of 2027, the changing macro environment will inevitably dictate a steady Yen appreciation from its current discounted levels.

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor.)

More than a million users rely on FXStreet for real-time market data, charting tools, expert insights, and forex news. Its comprehensive economic calendar and educational webinars help traders stay informed and make calculated decisions. FXStreet is supported by a team of about 60 professionals, split between the Barcelona headquarters and various global regions.

Read More