[TMGM Financial Breakfast] Gold Breaks Above $5,300 – Not a Speculative Mania, but a Structural Shift

Bởi Aiko Tanaka

Đã cập nhật: 2 Jul 2026

BÀI VIẾT PHỔ BIẾN

The Global Head of Commodity Research at Standard Chartered Bank noted that the core driver of this gold rally is a deep structural shift in the market, rather than a surge of speculative hot money.

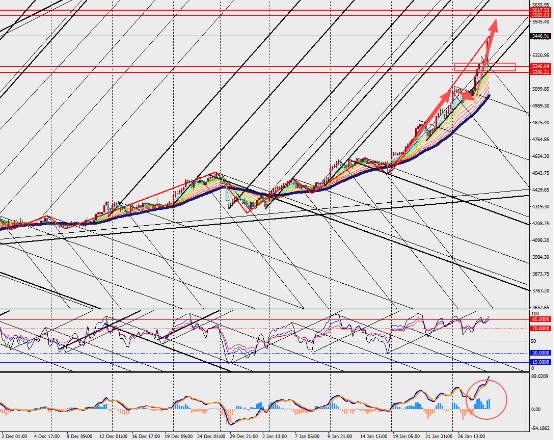

Spot gold has extended its strong uptrend, repeatedly printing fresh record highs, with prices now firmly holding above the $5,300 per ounce level.

Fundamentals remain the key pillar behind this unprecedented rally in gold. As of 20 January, tactical investors have indeed increased their gold exposure, but the pace of position-building has lagged far behind the speed of the price move. Over the past two weeks, net long positions in gold funds rose by 14,900 contracts, of which new long positions accounted for 14,800 contracts, while over the same period gold prices gained around $300 per ounce. Under normal market conditions, a 60,000-contract shift in positioning would typically only correspond to a price move of about $100 per ounce. This clearly suggests that other core forces are now driving gold’s price action.

The impact of traditional macro drivers on gold is fading, while structural drivers are becoming increasingly dominant. Growing concerns over the Federal Reserve’s independence, rising expectations for more room to ease monetary policy, elevated geopolitical risks, and renewed worries about trade and tariff frictions are all pushing mainly retail investors to accelerate their allocation into gold.

Tactical buying is not the primary engine of this rally. It is structurally driven allocation demand that is truly supporting gold’s upside. Currently, speculative positioning in gold accounts for 26.4% of open interest—relatively elevated, but still well below the historical peak of 47.9%. This suggests that positioning is not yet excessively crowded and the rally has not been fully “used up” by speculative flows.

The options market further reinforces the constructive short-term outlook for gold. One-month implied volatility has surged again, climbing back to its highest level since March 2022. At the same time, the one-month risk-reversal gauge has risen to its highest level since April 2024, and has consistently shown a clear skew in favour of call options.

In the physical gold space, demand for bars and jewellery remains robust. China continues to be the key pillar of global gold consumption, with Shanghai Gold Exchange prices once again trading at a premium. In years when consumption is strong, gold demand typically starts to pick up about six weeks before the Lunar New Year. In 2026, the domestic gold market has already been trading at a premium since the start of the year. This implies that even if prices pull back before the Lunar New Year, they are likely to find solid support.

Central bank gold purchases are also providing a firm floor for prices. In Q3 2025, global central bank buying of gold increased significantly, and preliminary data for Q4 suggest that appetite for gold reserves has not diminished. This behaviour is giving the gold market powerful downside protection.

Market Commentary:

Gold’s break above the $5,400 threshold is a reflection of a mature bull market driven by structural demand shifts, rather than a short-term spike fuelled by speculative trading. This pattern implies that even if volatility rises later on, gold is likely to remain underpinned by strong and lasting support.

Aiko Tanaka is our precious metals specialist with 10 years of experience in commodity markets. She holds a degree in Geology and professional certification in Commodity Market Analysis, covering gold, silver, platinum, and palladium markets with mining industry insights. Alongside her analysis, Aiko has authored thought-leadership pieces on commodities and contributes educational content aimed at new investors in the sector.

Đọc thêm