Gold’s Nearly 4% Weekly Drop Is Only the Beginning? Triple Pressure From the Dollar, Treasury Yields, and Rate Hike Expectations Still Far From Over

Bởi Aiko Tanaka

Đã cập nhật: 18 May 2026

BÀI VIẾT PHỔ BIẾN

Gold prices fell below the US$4,500 level as a stronger US dollar, surging Treasury yields, and escalating Middle East tensions continued to pressure the market. Rising oil prices have intensified inflation concerns, while market expectations for Federal Reserve rate hikes have strengthened significantly, placing additional pressure on non-yielding gold.

Against a backdrop of worsening geopolitical risks, traditional safe-haven asset gold is now competing with the US dollar and US Treasuries for defensive capital flows — and recently, the latter two have clearly become the preferred safe-haven assets.

The deadlock surrounding the US-Iran conflict is far from over. In fact, tensions continue to escalate.

UAE officials stated on Sunday that a nuclear power facility in the country caught fire following a drone attack, while Saudi Arabia reported intercepting three drones entering from Iraqi airspace.

These incidents suggest that although hostilities related to the Iran conflict have eased significantly since the April ceasefire agreement took effect, drone attacks launched from Iraq toward Gulf countries such as Saudi Arabia and Kuwait are still continuing.

The diplomatic deadlock is equally concerning.

In response to Iran’s proposals, the United States reportedly outlined five key conditions, including requiring Iran to transfer 400 kilograms of enriched uranium to the US and allowing only one Iranian nuclear facility to remain operational.

President Trump is expected to meet with senior national security advisors on Tuesday to discuss potential military options against Iran.

Meanwhile, the US Dollar Index recorded its largest weekly gain in two months.

The strength of the dollar has not occurred by accident — it has been driven largely by the continued surge in US Treasury yields.

The 10-year US Treasury yield climbed to 4.599%, sharply increasing the opportunity cost of holding gold.

Since gold itself generates no interest income, rising bond yields significantly reduce investor appetite for the precious metal.

At the same time, heavy corporate bond issuance aimed at financing artificial intelligence-related spending, combined with signs of accelerating US economic growth, has also contributed to higher yields.

This suggests that the current rise in yields reflects not only inflation expectations, but also improving demand conditions within the real economy.

Persistent inflation pressures are now reshaping market expectations for the Federal Reserve’s policy path.

According to CME FedWatch data, markets currently estimate a 49.5% probability that the Fed will raise rates by at least 25 basis points at its December meeting. Just one week ago, that probability stood at only 14.3%.

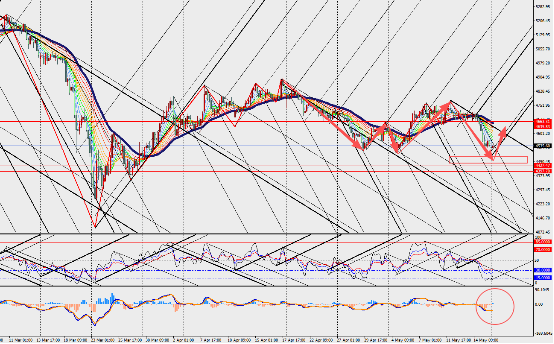

Market Analysis:

Gold is staging a technical rebound from oversold conditions on the 4-hour chart, while both the MACD lines and histogram are forming an expanding bullish crossover below the zero axis.

Market focus will continue to center on developments in the Middle East conflict and its impact on energy prices and bond yields.

However, the dominant narrative driving the gold market will likely remain the ongoing conflict in the Middle East and its transmission effects on oil prices and Treasury yields.

As long as energy supplies through the Strait of Hormuz remain largely disrupted, inflation pressures are unlikely to ease.

That means the shadow of further rate hikes will continue hanging over markets, while both the US dollar and Treasury yields are likely to remain major headwinds for gold prices.

Aiko Tanaka is our precious metals specialist with 10 years of experience in commodity markets. She holds a degree in Geology and professional certification in Commodity Market Analysis, covering gold, silver, platinum, and palladium markets with mining industry insights. Alongside her analysis, Aiko has authored thought-leadership pieces on commodities and contributes educational content aimed at new investors in the sector.

Đọc thêm