Crude Oil jumps as Tehran walks and Washington waves it off

Bởi Joshua Gibson

Đã cập nhật: 1 Jun 2026

BÀI VIẾT PHỔ BIẾN

Crude Oil spent all of May bleeding out a war premium on the assumption that a US-Iran deal was a formality, and on Monday the market got a blunt reminder that nobody actually signed anything.

- Iran suspended talks with the US and vowed to completely close the Strait of Hormuz.

- WTI rebounded sharply just ahead of the US session as the war premium snapped back.

- Tehran also threatened to activate the Bab el-Mandeb Strait through allied forces.

Crude Oil spent all of May bleeding out a war premium on the assumption that a US-Iran deal was a formality, and on Monday the market got a blunt reminder that nobody actually signed anything. West Texas Intermediate (WTI) spot opened near $88.00, which doubled as the day's low, then ripped higher into the US session to print a high close to $93.00 before settling near $91.00. The moment Tehran reached for the one lever it has used over and over, the tape repriced a conflict it had been told was effectively over. Both capitals are performing for their own audiences, and the market keeps mistaking the performance for progress.

The deal Tehran just walked away from

Here is where the skepticism toward the Iranian side earns its keep. The announcement that Iran would halt the exchange of messages through mediators and "completely" close the Strait of Hormuz came via state-affiliated outlet Tasnim, citing a statement it did not attribute to any named official. The stated trigger was Israel's expanded operation in Lebanon against Hezbollah, with Tehran insisting no dialogue resumes until Israel withdraws fully and halts attacks in Lebanon and Gaza. Strip the framing and the substance is familiar: this is the same Hormuz threat Tehran has brandished since the war began, recycled as leverage every time talks get uncomfortable. The waterway has been contested and largely shut to international shipping for months, so a pledge to "completely" close it reads less like escalation than a louder version of the status quo. The detail worth sitting with is that the draft memorandum of understanding (MOU) was still awaiting sign-off from both Trump and the newly installed Ayatollah Mojtaba Khamenei, who has not appeared in public since his appointment, and that Washington had tightened its terms on enriched uranium and the strait only days earlier. The deal was never as done as May's price action implied.

Washington's everything-is-fine routine

The US side deserves no less scrutiny. Trump ended the naval blockade of the strait on Friday, telling stranded ships they could start heading home, a clear de-escalation. By Monday, with Iranian state media saying talks were off, the White House line was that he had not heard of any such thing and that negotiations were "continuing at a rapid pace," alongside advice to "sit back and relax" because "it always works out." Pressed, he allowed it was "fine if they're done talking" and that Iranians are "better negotiators than they are fighters." That is the contradiction the consensus keeps glossing over: one side is publicly walking out while the other insists nothing has changed, and a market that wants the optimistic version is left to reconcile two accounts that cannot both be true. When official messaging and the counterparty's own statements diverge this far, the war premium belongs back in the price, not out of it.

A second chokepoint waved around again

The Bab el-Mandeb angle is the tell that this is leverage, not a plan. Tehran's statement also floated activating "other fronts," naming the Bab el-Mandeb Strait, the Red Sea chokepoint where Iran-aligned forces have disrupted traffic before. That threat has been dusted off repeatedly since the spring without being executed at scale, and bundled with the Hormuz pledge it looks calibrated for the headline rather than the damage. The arithmetic still gives it teeth: roughly a fifth of global oil moves through Hormuz and a meaningful slice of seaborne crude through Bab el-Mandeb, so a credible threat to both keeps a fear bid under the market regardless of follow-through.

Premium bleeding, not gone

The daily chart frames why this still matters. Even after May's slide, WTI is rallying straight back into its 50-day Exponential Moving Average (EMA) near $92.00, the pivot it lost late last month, and sits far above the 200 EMA close to $77.50. Zoom out and the contrast is starker: spot is miles below the war-spike peak above $113.00 from early March, yet still well north of the roughly $62.00 base that held before the conflict. The premium has bled substantially from the highs but is nowhere near gone, and Monday's move shows how fast the market will try to rebuild it when Tehran rattles the strait. The daily Stochastic Relative Strength Index (Stoch RSI) near 32 is curling up from the lower half of its range, leaving room to run if the headlines keep coming.

Levels and the trade

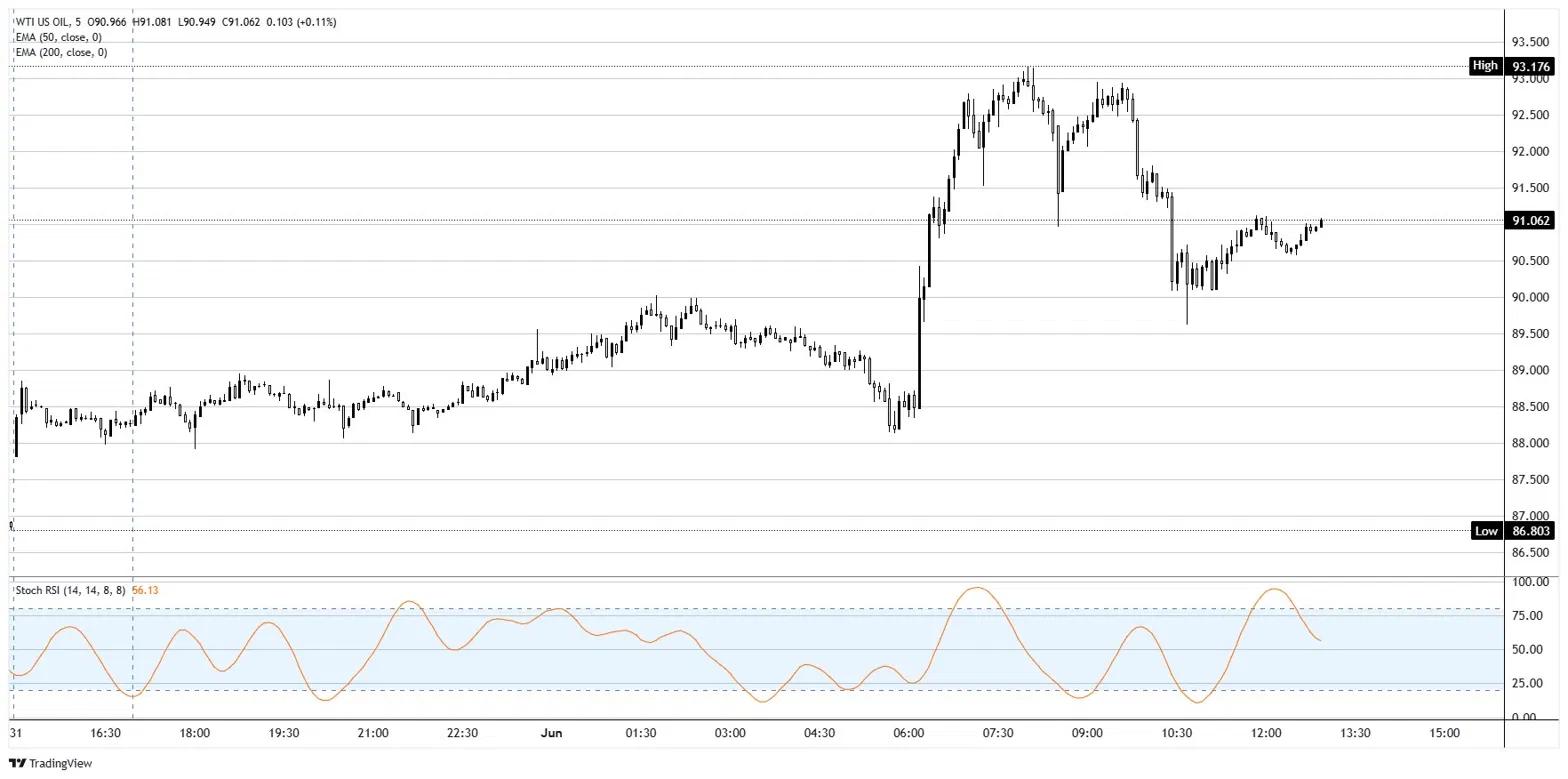

The jump that mattered came in the hours ahead of the US session, with WTI accelerating off the $88.00 open toward $93.00 as the Tasnim headline crossed, then easing back near $91.00. Brent futures, the more widely watched global benchmark, pushed toward $97.00 from around $93.00 earlier on the same news. Bias leans higher while talks stay frozen and the Hormuz threat is live, but this is a headline tape, not a trend, and it can reverse on a single social media post. The $92.00 to $93.00 zone, where the 50 EMA meets the day's high, is the wall to clear; a daily close above it says the market is rebuilding war premium in earnest. On the downside, $88.00 is first support, and a break that holds below it says the rebound has failed. Fade strength into the $92.00 to $93.00 resistance unless an actual disruption materializes, because in this regime the only thing that matters is the difference between a threat and an event, and so far this is still a threat.

WTI 5-minute chart

WTI Oil FAQs

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

OPEC (Organization of the Petroleum Exporting Countries) is a group of 12 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

Hơn một triệu người dùng dựa vào FXStreet để có dữ liệu thị trường thời gian thực, công cụ biểu đồ, góc nhìn chuyên gia và tin tức Forex. Lịch kinh tế toàn diện và các hội thảo web giáo dục giúp nhà giao dịch luôn cập nhật và đưa ra quyết định có tính toán. FXStreet có khoảng 60 nhân sự, chia giữa trụ sở Barcelona và nhiều khu vực toàn cầu.

Đọc thêm