[TMGM Financial Breakfast] JPMorgan: Gold Is Not an Effective Hedge but Should Be Viewed as an Investment Asset

作者 Aiko Tanaka

更新: 13 Apr 2026

熱門文章

JPMorgan argues that gold should not be regarded as a reliable hedging tool, but rather as an investment asset, as its correlation with equities and other risk assets has historically been inconsistent.

According to JPMorgan, the sharp sell-off in gold during the U.S.–Iran conflict has weakened its role as a defensive hedge within investment portfolios. Instead, investors should treat gold as an investment asset rather than a risk hedge.

Over the 20 days following the Iranian attack, gold prices fell from a peak of $5,415 per ounce to a low of $4,100, representing a decline of approximately 24%. Although prices have since rebounded significantly, gold has struggled to build sustained upward momentum as the conflict continues.

Despite its poor track record in geopolitical events over the past 30 years, many investors still consider gold a hedge against geopolitical risk. However, even beyond such shocks, gold faces several structural challenges. Its volatility is comparable to that of emerging market equities, and unlike other assets, gold does not generate income. While investors may have overlooked this lack of yield during the past two years, the opportunity cost of holding gold remains an important consideration.

JPMorgan notes that holding gold can be justified when based on fundamentals such as central bank buying or as a hedge against currency debasement. However, using gold as a tool to offset market drawdowns is less reliable.

Despite these limitations, there are still strong reasons to hold gold. Central banks continue to accumulate gold as part of efforts to diversify reserves away from the U.S. dollar. In addition, investors are allocating to gold as a hedge against rising government debt and rapid expansion in money supply. With limited supply growth, gold retains intrinsic investment value — reinforcing the view that it is an asset, not a hedge.

JPMorgan maintains a bullish long-term outlook on gold, viewing recent pullbacks as temporary. Over the past five years, gold has surged more than 170%, driven largely by geopolitical volatility and increasing global fragmentation. Concerns over currency debasement, economic growth, inflation, and fiscal sustainability have also supported demand for the precious metal.

Bearish views on gold focus primarily on two risks. First, central banks may slow or halt their gold-buying activity. Second, retail investors may reduce their exposure to gold.

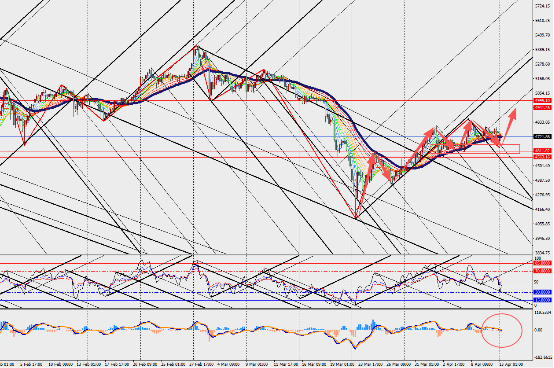

Market Interpretation:

On the four-hour chart, gold is showing a rebound following a recent decline, with MACD lines and volume bars converging near the zero axis. Although the current rally is unlikely to be linear, the broader upward trend remains intact.

Long-term drivers, including official reserve accumulation and investor diversification into gold, continue to support the outlook, suggesting further upside potential over time.

Aiko Tanaka is our precious metals specialist with 10 years of experience in commodity markets. She holds a degree in Geology and professional certification in Commodity Market Analysis, covering gold, silver, platinum, and palladium markets with mining industry insights. Alongside her analysis, Aiko has authored thought-leadership pieces on commodities and contributes educational content aimed at new investors in the sector.

閱讀更多