[TMGM Financial Breakfast] Middle East Conflict Reignites Inflation Fears! Is Gold’s Latest Pullback a Buying Opportunity or the Beginning of a Bear Market?

Bởi Aiko Tanaka

Đã cập nhật: 4 Jun 2026

BÀI VIẾT PHỔ BIẾN

On Wednesday, gold prices retreated sharply as escalating tensions in the Middle East rattled markets. US airstrikes near the Strait of Hormuz and Iranian attacks on Kuwait sent oil prices soaring and inflation expectations higher. Markets have significantly increased expectations for future Federal Reserve rate hikes. Although gold faces short-term pressure, ongoing geopolitical uncertainty and its long-term safe-haven appeal continue to provide support.

The latest escalation in Middle East tensions has once again become the primary focus of financial markets. The United States carried out airstrikes near the Strait of Hormuz, while Iran launched attacks on Kuwait, damaging local airport infrastructure and causing casualties. Diplomatic efforts aimed at easing tensions have made little progress so far, and negotiations between Iran and the United States remain deadlocked. Iran’s Foreign Minister explicitly stated that if Israel continues military operations in Beirut, Iran will resume hostilities.

Volatility in the gold market is being driven primarily by escalating tensions between the United States and Iran. As the conflict intensifies, rising energy prices have become almost inevitable, significantly increasing global inflation expectations. The energy shock is now rapidly spreading into both the services sector and manufacturing industries. Beyond geopolitical factors, strong US economic data has further reinforced expectations for a prolonged high-interest-rate environment.

According to data from the Institute for Supply Management (ISM), the US Services Prices Paid Index rose to its highest level in nearly four years during May, with businesses widely reporting surging costs for petroleum-related products. Many companies cited higher fuel surcharges and increased resin costs and indicated plans to pass those expenses on to consumers. The conflict has now lasted for three months, creating disruptions to commodity supply chains that have far exceeded earlier expectations and stand in sharp contrast to the peace dividend many investors had anticipated before the conflict erupted.

Wednesday’s ADP National Employment Report showed that US private-sector employment increased by 122,000 jobs in May, exceeding market expectations of 117,000. Earlier April data also showed a significant increase in job openings. Meanwhile, the Services PMI rose from 53.6 to 54.5, beating expectations, while both new orders and inventory indicators rebounded sharply. Factory orders surged 4.8% month-on-month, marking the strongest increase in an extended period.

The President of the New York Federal Reserve stated that current monetary policy remains appropriately positioned and argued that inflation risks stemming from the Middle East conflict are unlikely to persist for an extended period, making immediate policy adjustments unnecessary. However, markets remain unconvinced. Investors have already fully priced in approximately 19 basis points of Federal Reserve tightening before December, while the probability of a full 25-basis-point rate hike by March next year is also largely reflected in market pricing.

The upcoming May Non-Farm Payrolls report will become a critical market indicator. If employment data remains strong, it could encourage the Federal Reserve to shift away from its current dovish bias and reopen discussions surrounding a new rate-hike cycle. Such a development would support the US dollar while creating continued pressure on gold prices.

Investors should closely monitor Friday’s US Non-Farm Payrolls report, developments in Middle East diplomacy, and oil-price movements. If payroll data significantly exceeds expectations and ceasefire negotiations fail to make meaningful progress, gold could continue testing lower support levels. Conversely, if geopolitical tensions begin easing, gold may stage a technical rebound.

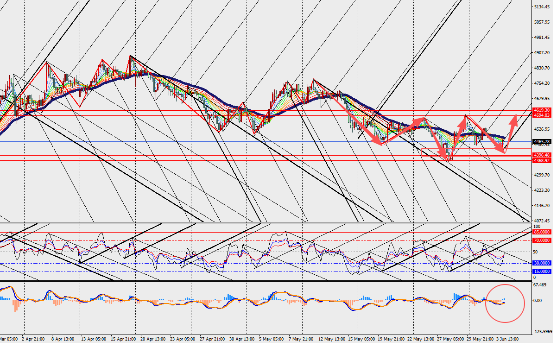

Market Analysis:

Gold rebounded after recent declines on the 4-hour chart timeframe, while both the MACD lines and histogram continued expanding near the zero axis. The gold market is currently caught in an intense battle between geopolitical risks, inflation expectations, and monetary policy dynamics. Short-term volatility is likely to remain elevated, but gold’s strategic allocation value remains worthy of attention. Investors should remain cautious and continue closely monitoring key economic data and geopolitical developments.

Aiko Tanaka is our precious metals specialist with 10 years of experience in commodity markets. She holds a degree in Geology and professional certification in Commodity Market Analysis, covering gold, silver, platinum, and palladium markets with mining industry insights. Alongside her analysis, Aiko has authored thought-leadership pieces on commodities and contributes educational content aimed at new investors in the sector.

Đọc thêm